Writing

Venture EDU

This started as a set of slideshows for internal education, but thought I’d outsource it with some text to interleave slides.

Note: AI was used in the making of the transitions.

The best startup diligence usually begins with an uncomfortable question. What does this company actually control? Not what it markets, not what its demo makes obvious, and not what the pitch deck claims. What does it control in the system around it?

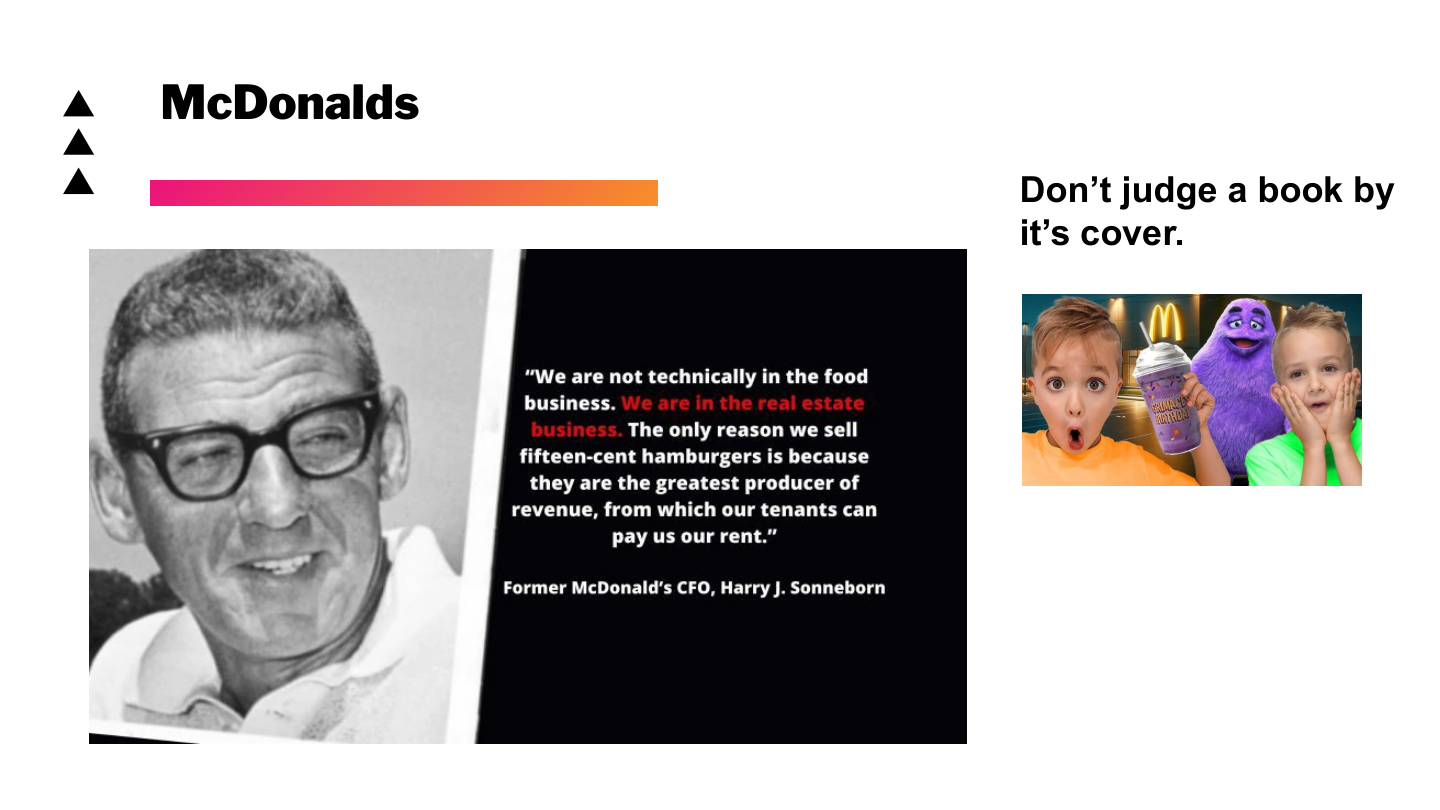

That is why the first example is McDonald’s. The point is not burgers. The point is that a company can look like one thing on the surface and compound value through something else entirely.

The Business Under the Business

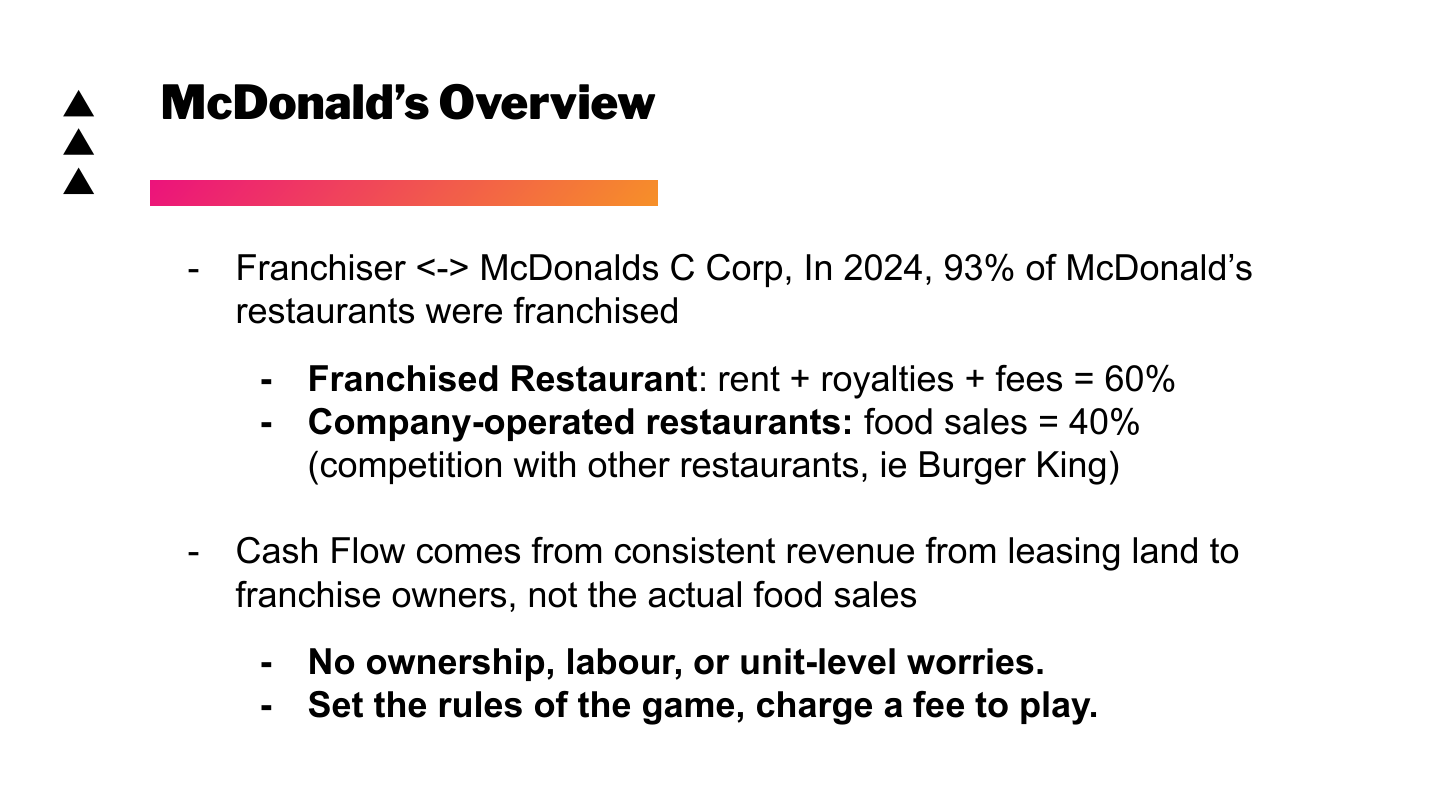

McDonald’s is a useful mental model because the visible product is almost a distraction. Customers experience fries, drive-throughs, and brand consistency. Franchisees experience operating leverage and a proven demand engine. But the corporate entity compounds through a real estate and franchise model that shifts many local operating burdens away from the parent company.

The lesson for startup diligence is that a business model can be stronger than the product it sells. McDonald’s sells food, but the durable machine is rent, royalties, fees, brand control, and standardized distribution. That model makes the company less exposed to the chaos of individual restaurants than it would be if it owned every local operational detail directly.

The Sonneborn model is the cleanest version of the idea: control the bottleneck, set the rules, and let other people operate inside the system. McDonald’s can own or master-lease the land and buildings, then rent them to franchisees at a markup. The franchisee takes on the day-to-day work; the parent company controls the terms of participation.

When evaluating startups, this is the kind of inversion worth looking for. The thing that looks like the product is often just the wedge. The real company may be a distribution network, a regulatory position, a workflow lock-in, a data asset, a financing mechanism, or a control point inside a market.

Why Diligence Exists

Venture diligence is not about proving that a company is good. It is about making a high-uncertainty decision less random.

In a fund context, diligence supports an investment decision. The goal is to understand whether the company can produce venture-scale returns, and whether the current price leaves enough room for that outcome. In an ecosystem or accelerator context, the goal can be slightly different: find companies that are worth learning from, working with, and helping compound.

Either way, diligence should move from surface area to mechanism. What problem is being solved? Who pays? Why now? Why this team? What changes if the company succeeds? What has to be true for the business to scale without breaking?

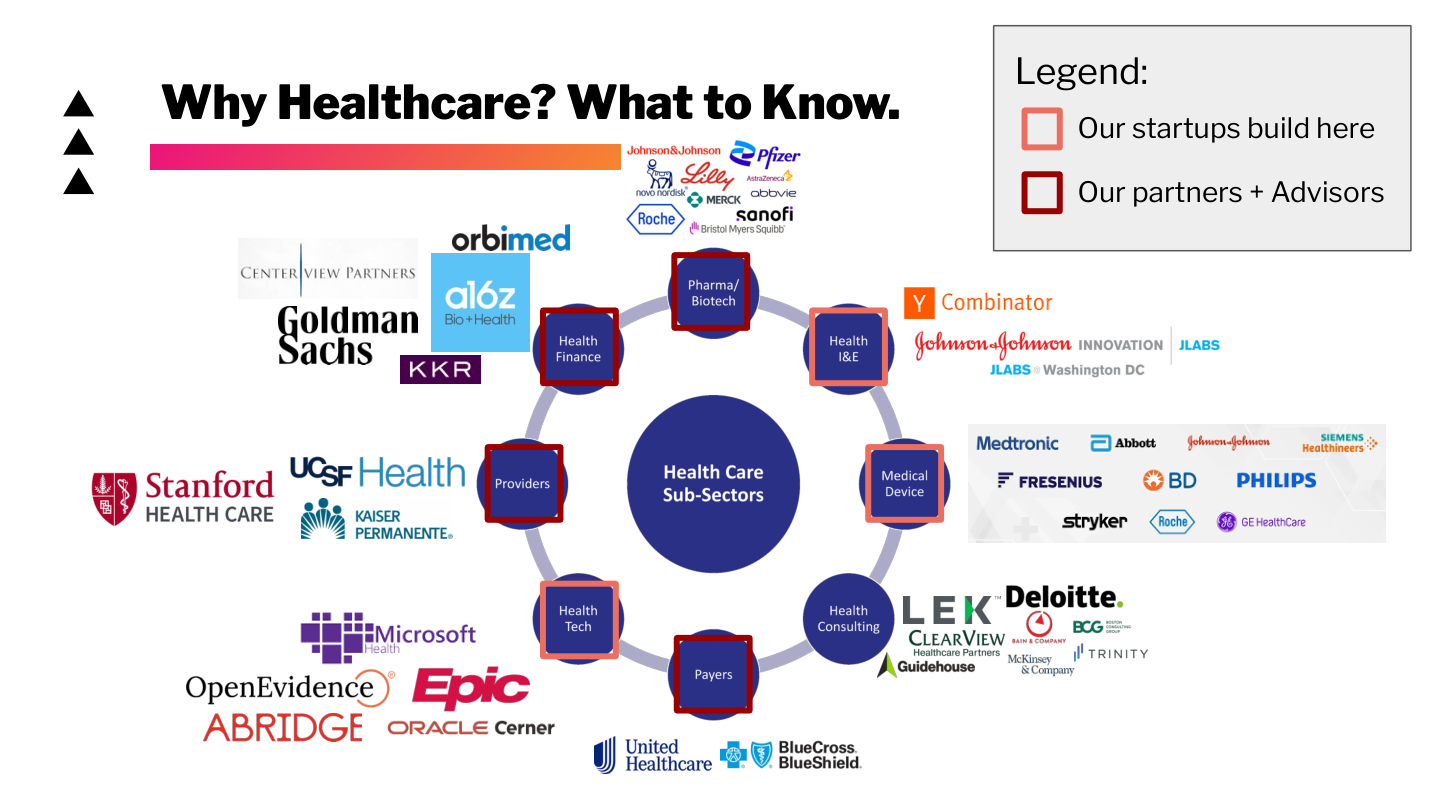

Healthcare Is Its Own Game

Healthcare startup diligence is especially tricky because the end user is often not the buyer, the buyer is often not the payer, and the payer is often optimizing for constraints that are invisible from the outside.

That means a healthcare startup can be technically impressive and still commercially weak. It can have a real clinical problem, a beautiful product, and a founder with taste, but still lose because reimbursement is unclear, procurement is brutal, integration is painful, or the economic buyer does not care enough to change behavior.

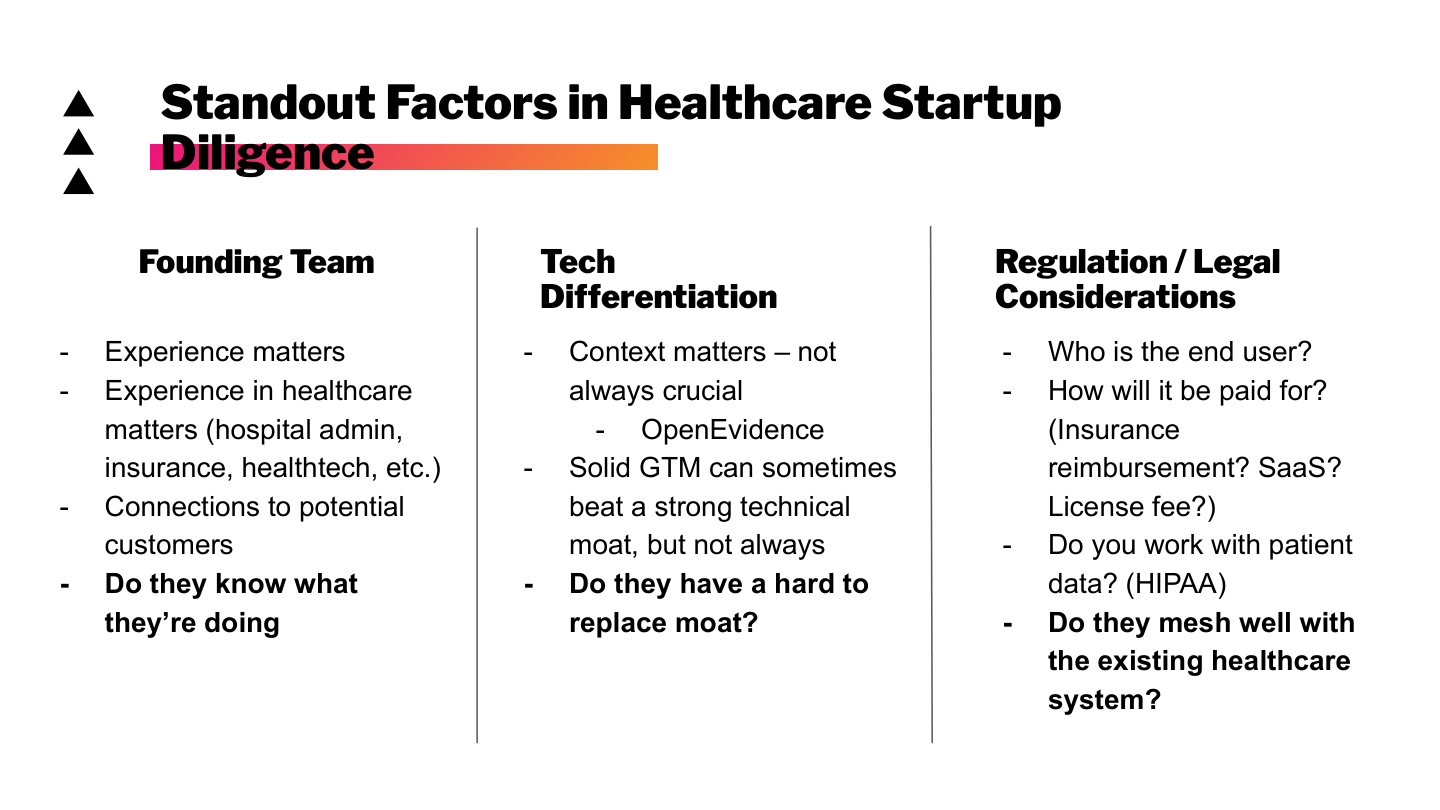

The key questions usually cluster into three categories.

First, the founding team. Healthcare is not a market where generic competence always transfers cleanly. Context matters: hospital administration, payer contracting, clinical workflows, broker channels, compliance, and customer relationships all shape whether a company can sell.

Second, differentiation. A technical moat matters, but in healthcare a distribution moat can matter more. Sometimes the winning company is not the one with the best model, algorithm, or product surface. It is the one that already fits into a hospital’s budget cycle, a payer’s claims flow, or an employer’s benefits process.

Third, regulation and legal structure. Who is the end user? Who pays? Does the product touch patient data? Does it need reimbursement? Does it work with the existing system, or does it require the system to behave in a way it historically refuses to behave?

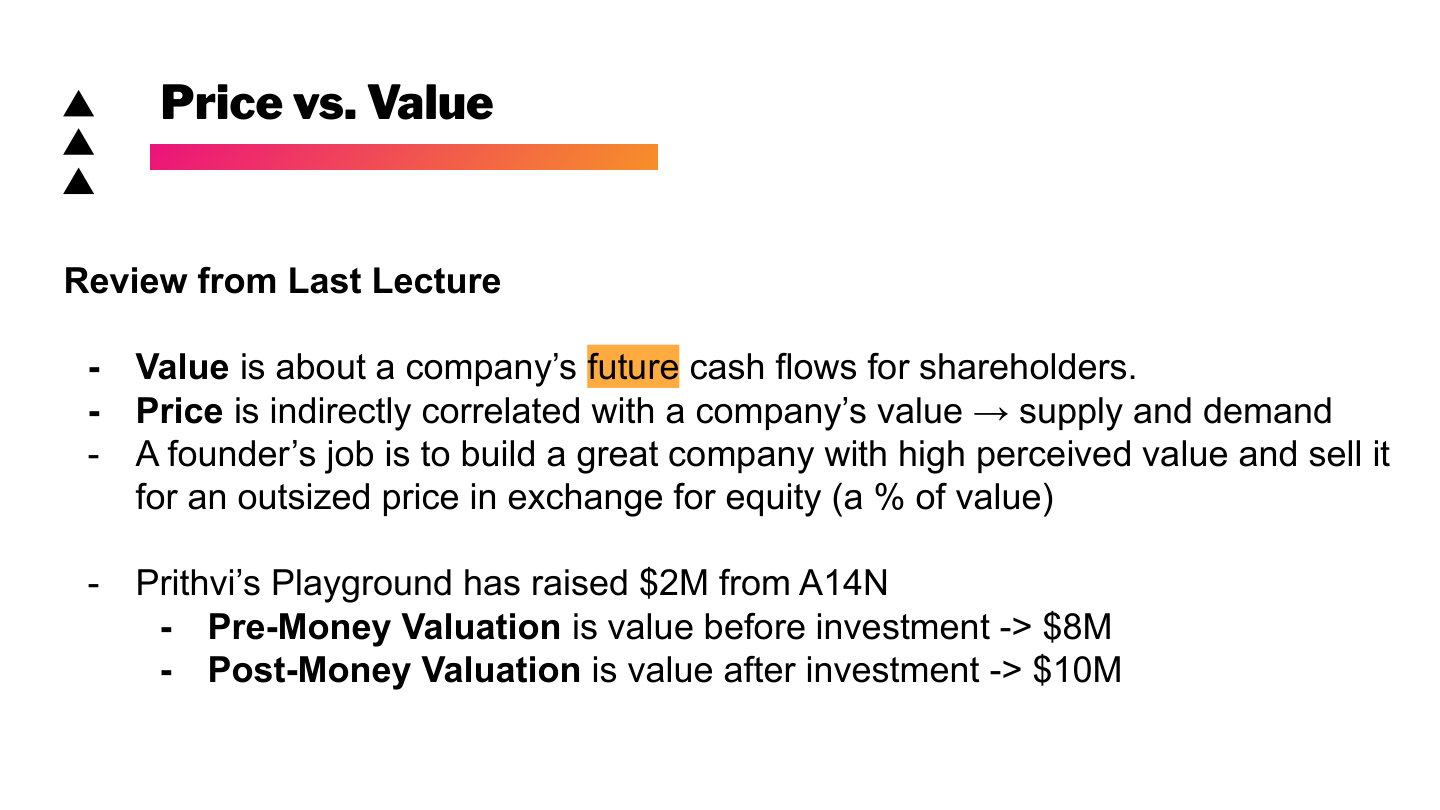

Price, Value, and Scaling

Venture investing is a bet on value creation, but the entry price determines how much of that value remains available to the investor. A great company can still be a bad investment if the valuation already assumes perfection.

Pre-money and post-money valuation are basic mechanics, but they matter because they force you to separate value from price. Value is tied to future cash flows and strategic importance. Price is what the market currently agrees to pay for a share of that value.

The gap between those two concepts is where venture gets interesting.

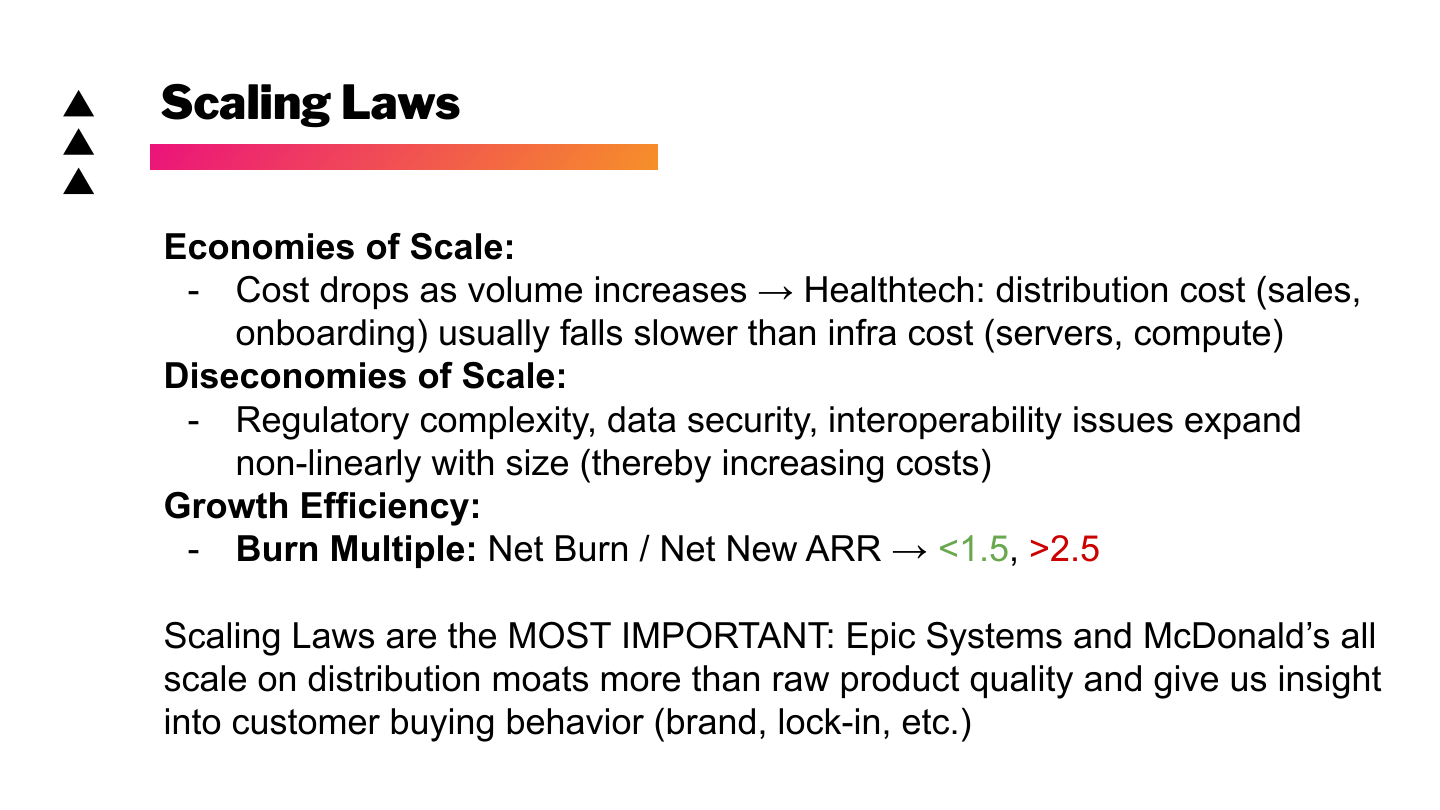

Scaling laws are the part most people underweight. Software businesses are attractive because marginal software costs can fall quickly. Healthcare businesses are harder because distribution, trust, compliance, sales, onboarding, and interoperability costs often do not fall as cleanly.

In healthtech, “can this scale?” often means “can this scale through the actual buying behavior of healthcare institutions?” Epic and McDonald’s are oddly useful comparisons here. Both show that distribution, lock-in, standardization, and customer behavior can matter more than raw product quality.

Inconvenient Truths About Healthcare

The healthcare system is not merely inefficient. Some of the inefficiency is structural, and some of it is economically useful to incumbents.

Consistency can matter more than cheapness. In healthcare, variance is dangerous. Hospitals, insurers, employers, and administrators often prefer predictable cost structures over theoretically lower prices that introduce volatility. That helps explain why narrow networks, prior authorization, and other frustrating systems persist. They are not only bureaucratic artifacts; they are tools for controlling variance, utilization, and channel economics.

Insurance incentives are also not the same as normal consumer incentives. Medical loss ratio rules cap profits as a percentage of premiums, which means cutting costs does not always create the incentive outsiders expect. In many cases, the system stabilizes around ratios rather than pure efficiency.

Another humbling truth: old technology can be more interoperable than new technology. Fax machines, phone calls, and paper workflows survive because they work across fragmented systems. A startup that mocks the old workflow without understanding why it persists will usually misread adoption risk.

The patient is also rarely the only economic buyer. Employers choose plans. Insurers design networks. PBMs shape formularies. Hospital committees approve devices. Patients experience the system, but they often do not control the purchasing decision.

This is why healthtech diligence has to ask not only “does this help patients?” but also “who has budget, authority, and incentive to make this change happen?”

Case Study: Venteur

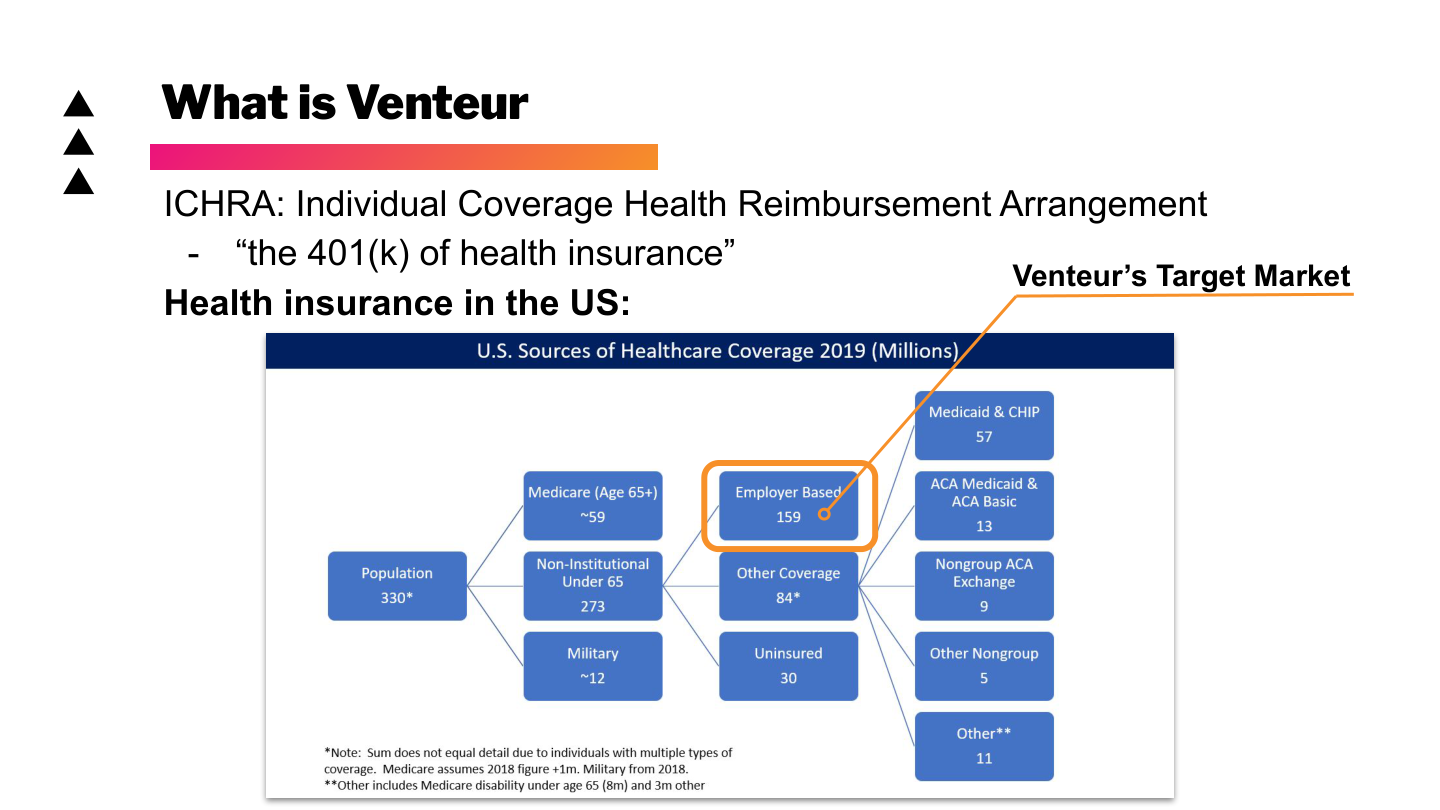

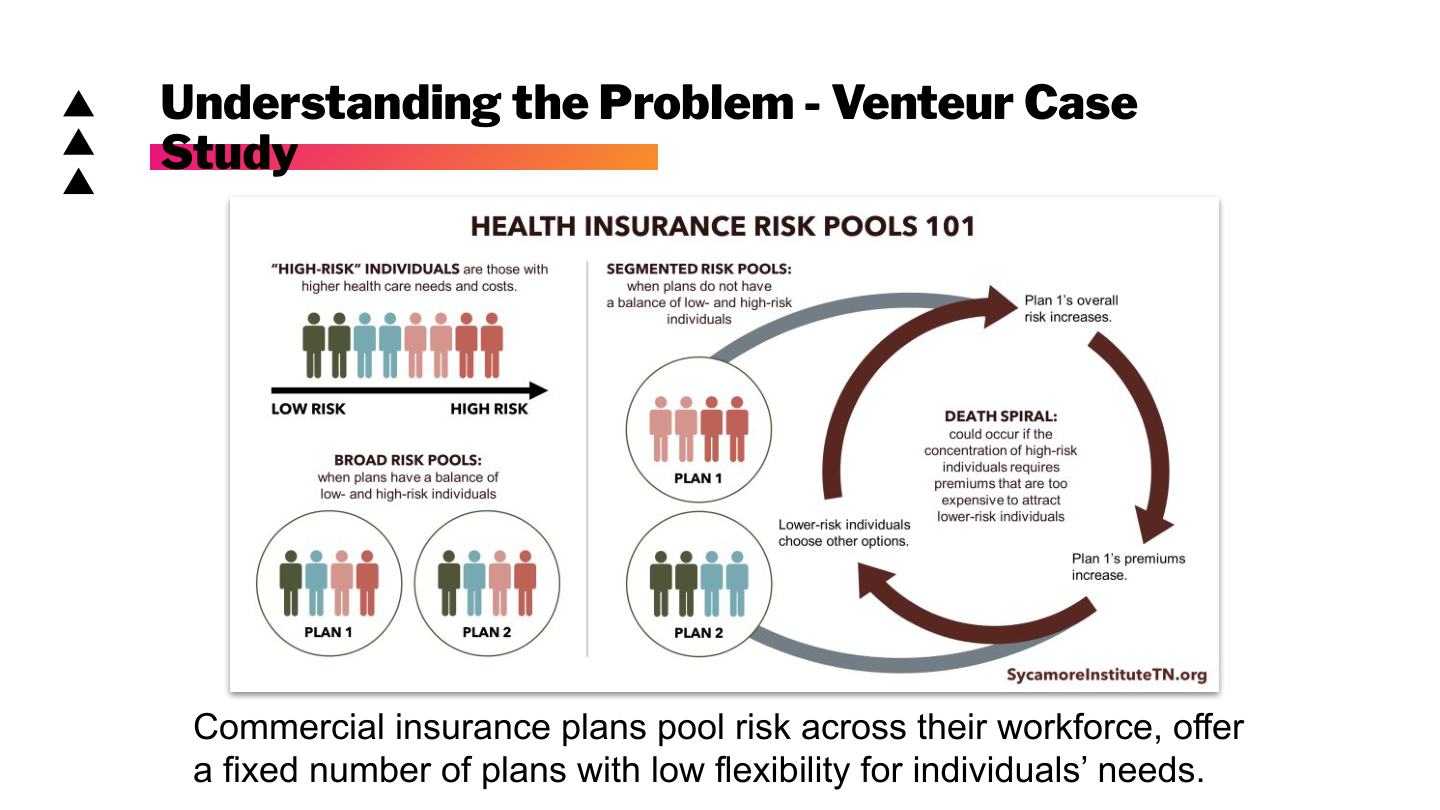

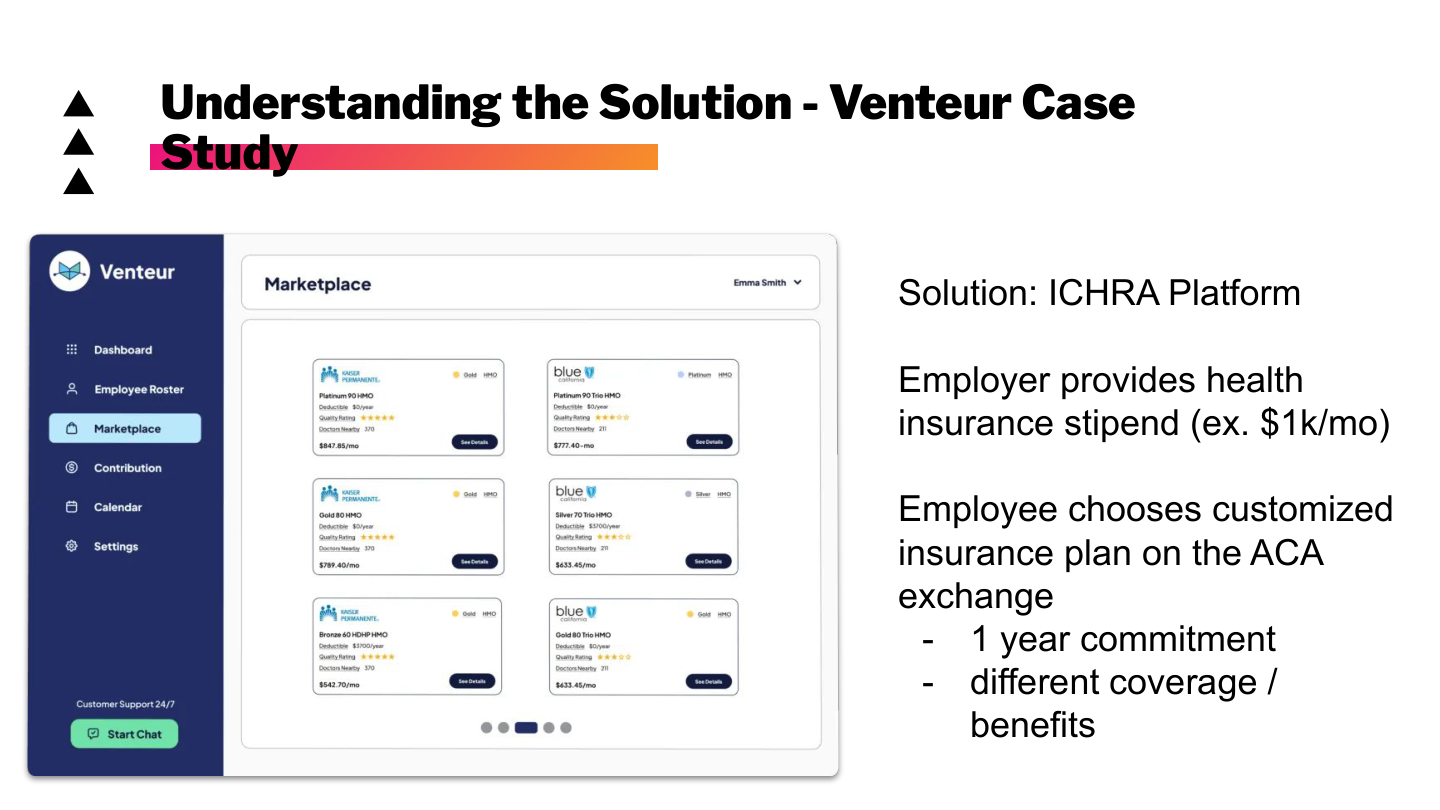

Venteur is a good case study because it sits inside a messy but important benefits transition: the move from one-size-fits-most employer insurance toward more flexible individual coverage arrangements.

The relevant acronym is ICHRA: Individual Coverage Health Reimbursement Arrangement. The simple version is that an employer gives an employee a health insurance stipend, and the employee uses it to choose an individual plan.

That model has an intuitive analogy: the “401(k) of health insurance.” Instead of the employer selecting a small number of group plans for everyone, the employer contributes dollars and the employee chooses a plan that better matches their own needs.

Start With the Problem

The first diligence move is to define the problem space precisely.

For Venteur, the problem is that commercial insurance pools risk across a workforce and offers a limited number of plans. That can be convenient for employers, but it creates poor fit for individuals. Different employees have different doctors, prescriptions, family structures, locations, and risk preferences. A small menu of plans cannot optimize for all of them.

But identifying pain is not enough. In venture, the pain must be severe enough to justify adoption. If the status quo is annoying but tolerable, switching costs can kill the company. A solution must be meaningfully better, not just cleaner in a deck.

Then Understand the Solution

The next question is whether the solution is a feature, a workflow, a platform, or a system-level wedge.

Venteur’s solution is an ICHRA platform. The employer provides a defined contribution, employees choose individual plans on the ACA exchange, and the platform handles the workflow that makes this administratively feasible.

The diligence question is not just whether this is useful. It is whether the company can own enough of the workflow to become durable. Does it integrate with HR and payroll? Does it reduce employer administrative burden? Does it build a broker channel? Does it improve employee plan selection enough to make the change feel obvious?

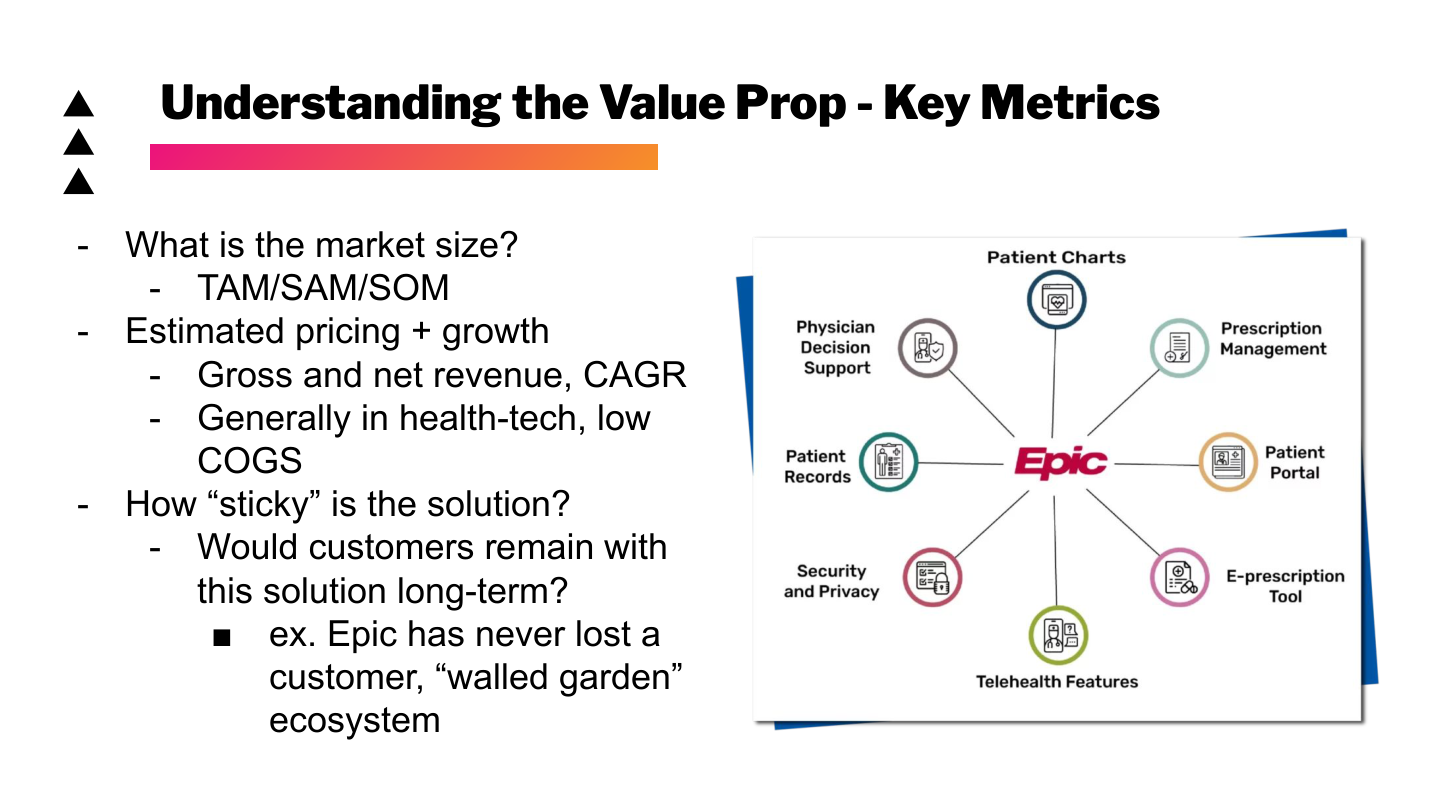

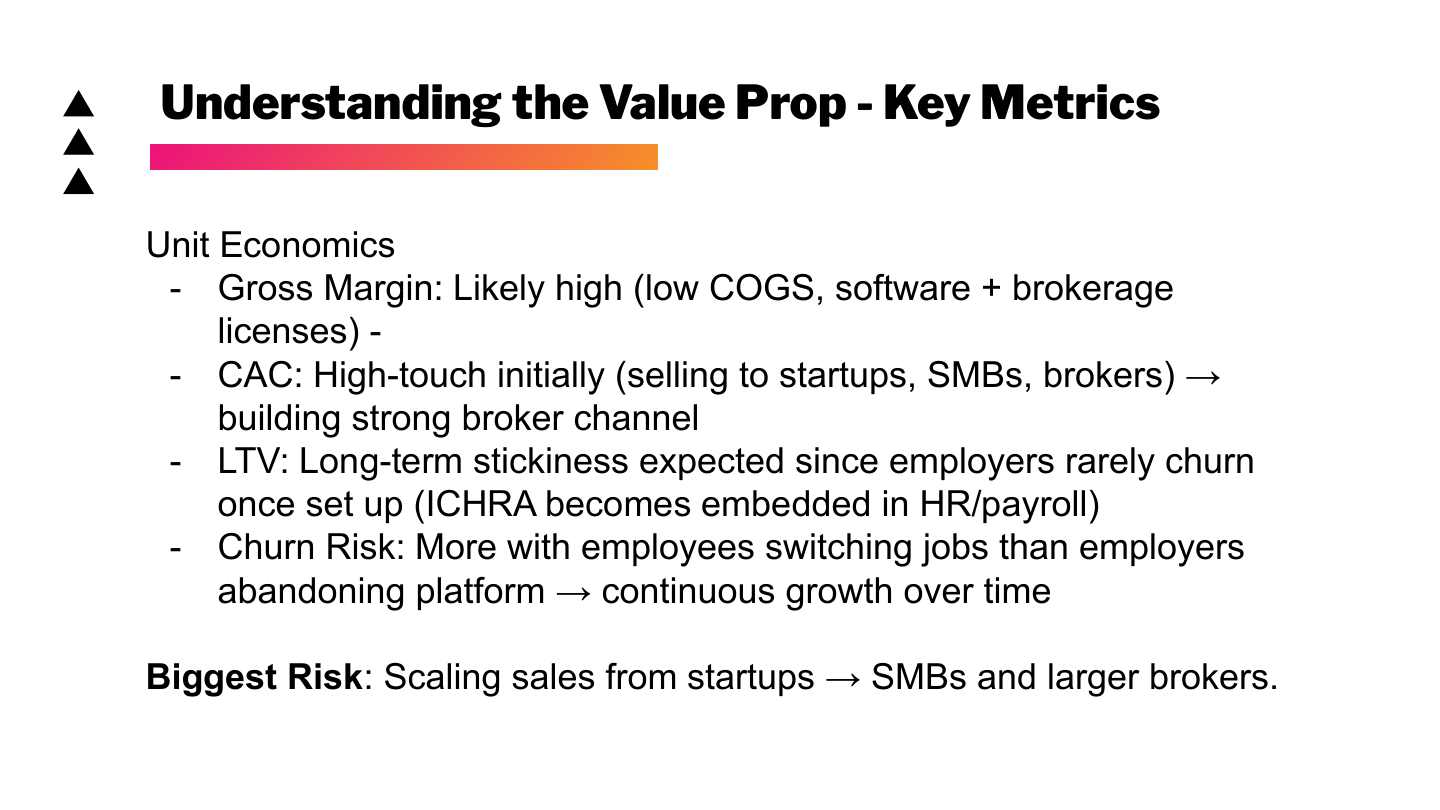

Value Proposition and Unit Economics

A startup can solve a real problem and still fail to become a venture-scale company. That is why the value proposition has to be translated into market size, pricing, growth, retention, gross margin, CAC, and LTV.

For healthtech software, gross margins are often attractive, but CAC can be dangerous. Selling into healthcare, benefits, and employers can require trust, education, channel partnerships, and long sales cycles. The question is whether the company can turn early high-touch selling into repeatable distribution.

In Venteur’s case, the upside is potential stickiness. Once an employer has embedded a benefits platform into HR and payroll, churn may be low. The risk is whether the company can scale from startup and SMB customers into larger channels without sales costs overwhelming the model.

Kill Questions

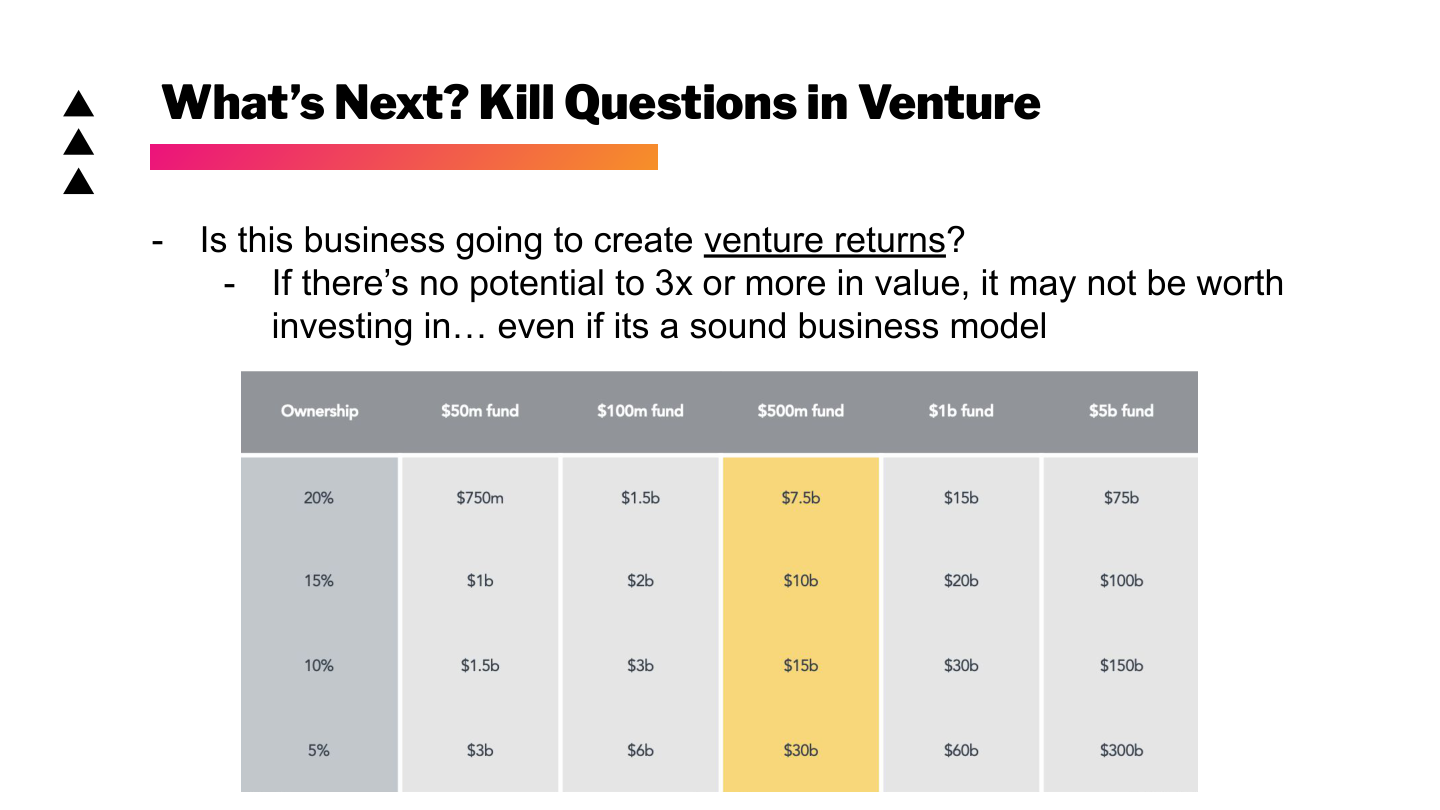

The hardest venture question is often not “is this a good business?” It is “can this produce venture returns?”

Plenty of companies are useful, profitable, and admirable without being venture-backable. Venture capital needs outlier outcomes because fund math depends on a small number of investments returning a large share of the fund.

That means the exit path matters from the beginning.

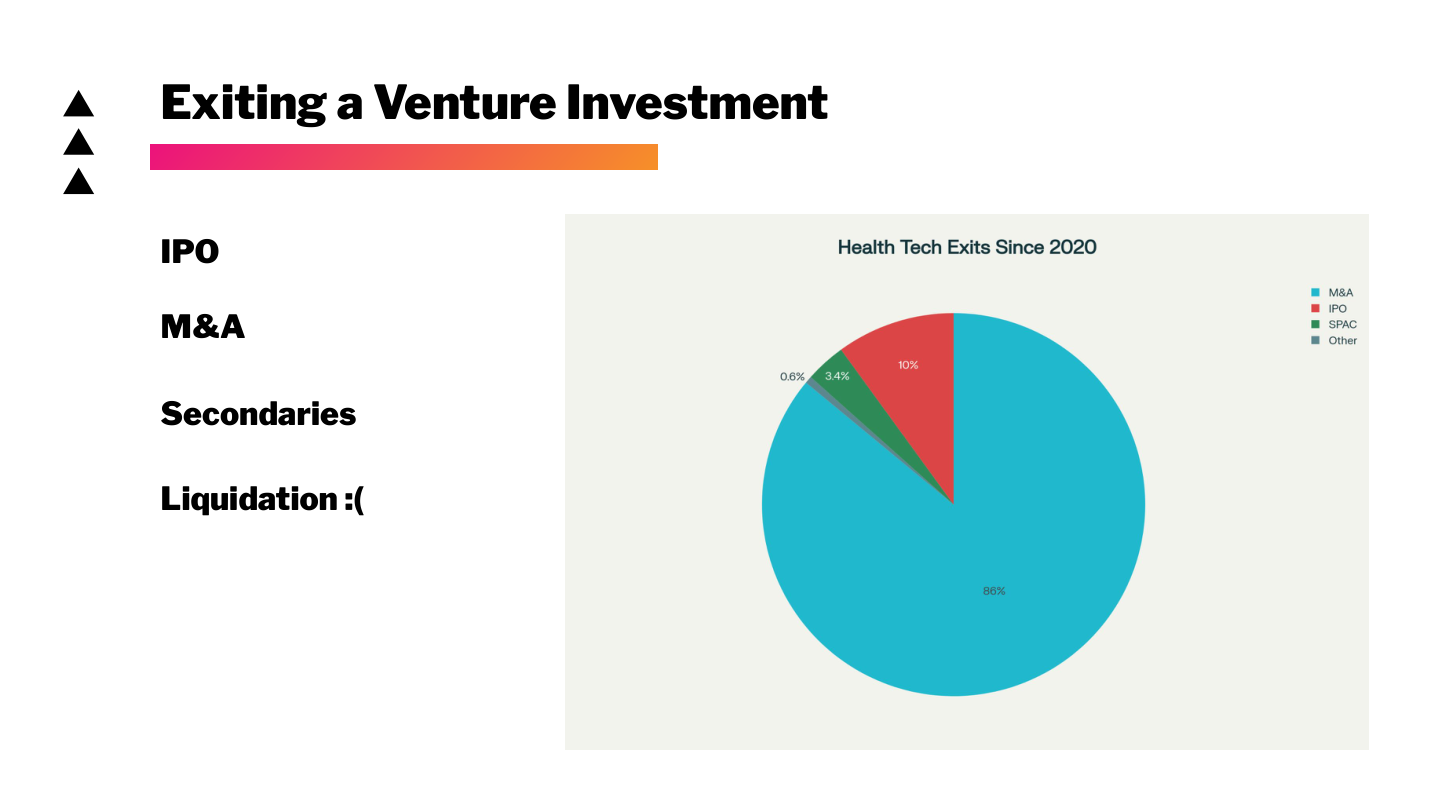

The standard paths are IPO, acquisition, secondaries, or liquidation. Only some of those outcomes produce the kind of return that justifies early-stage risk.

This is also why diligence can feel harsh. A company may deserve to exist, and still not fit the return profile of a venture fund.

How to Learn Diligence

The practical advice is simple: read and talk to people.

Reading gives you vocabulary. Conversations give you calibration. The best diligence instincts usually come from repeated exposure to how founders, customers, operators, investors, and incumbents describe the same market differently.

The AI Infrastructure Loop

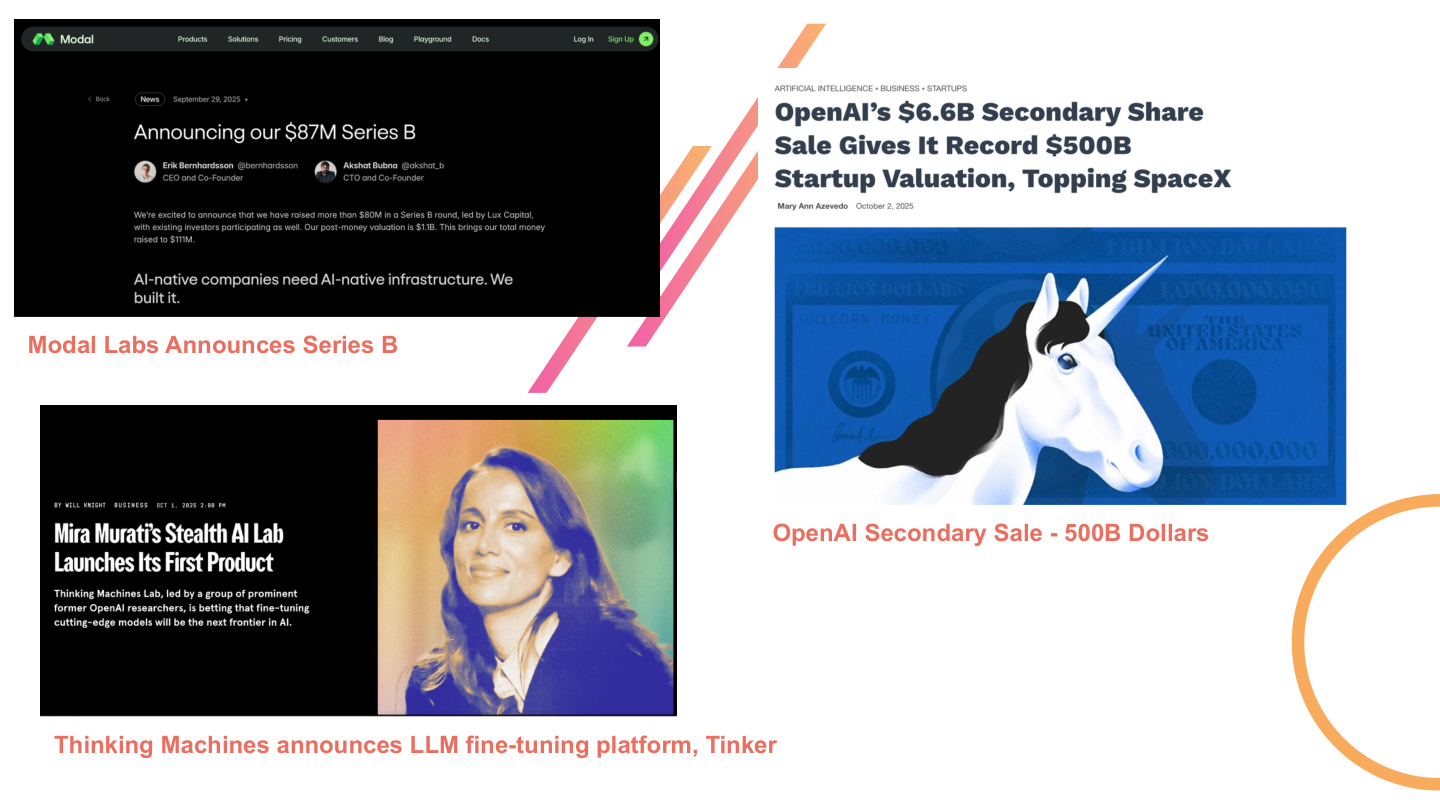

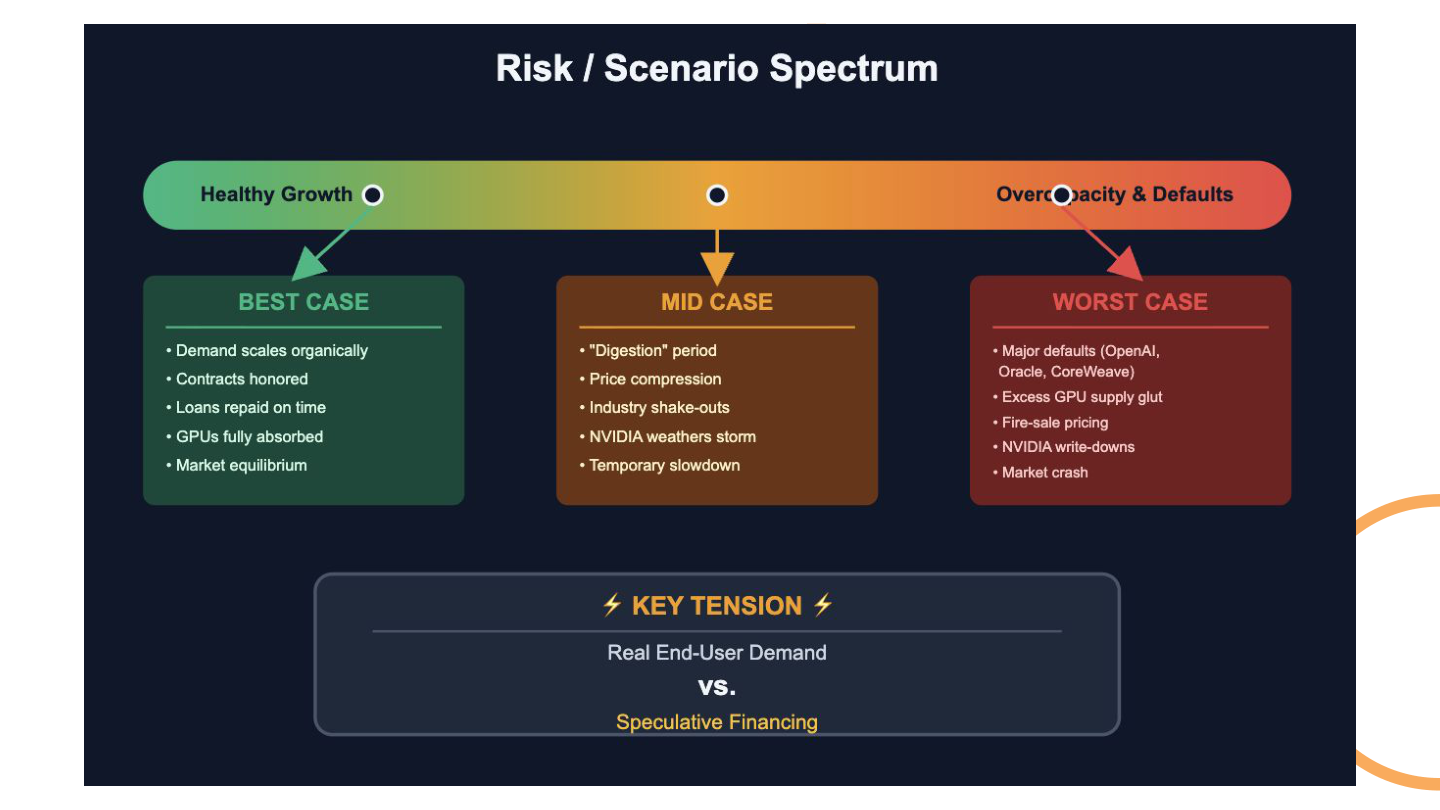

The deck then moves from healthtech diligence into a broader question about venture markets today. AI has changed the center of gravity in private markets, but the same diligence principles still apply: look underneath the obvious product and inspect the financing, incentives, and control points.

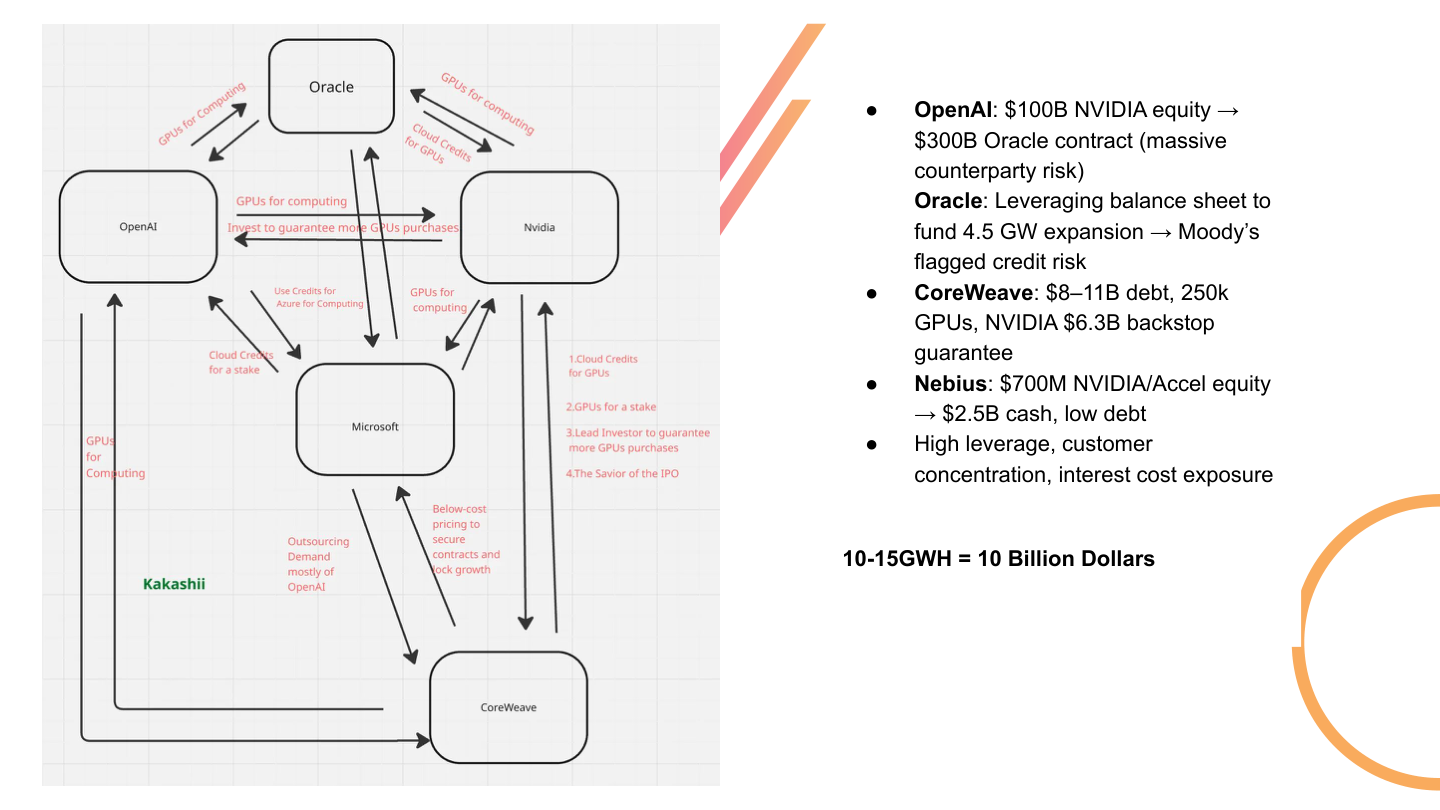

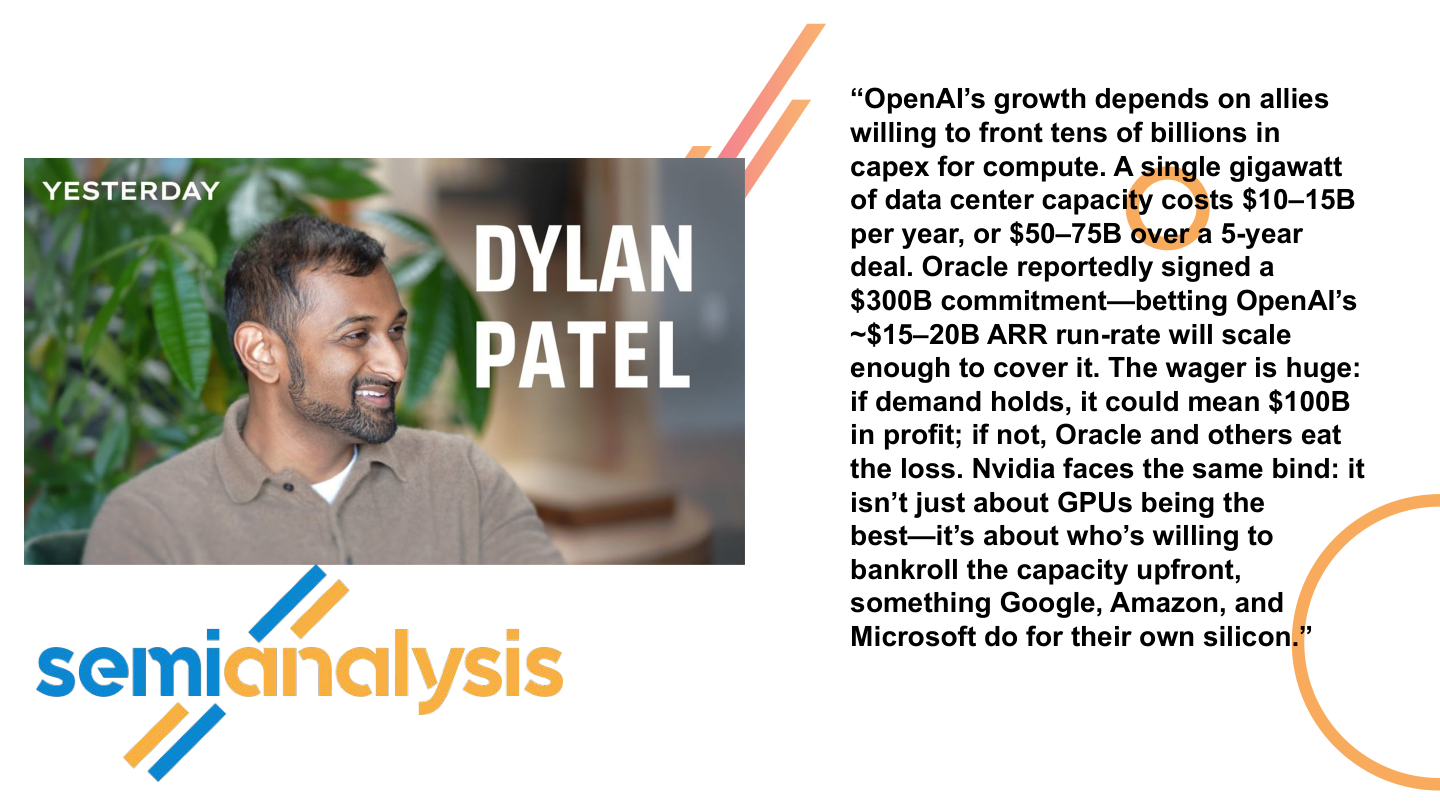

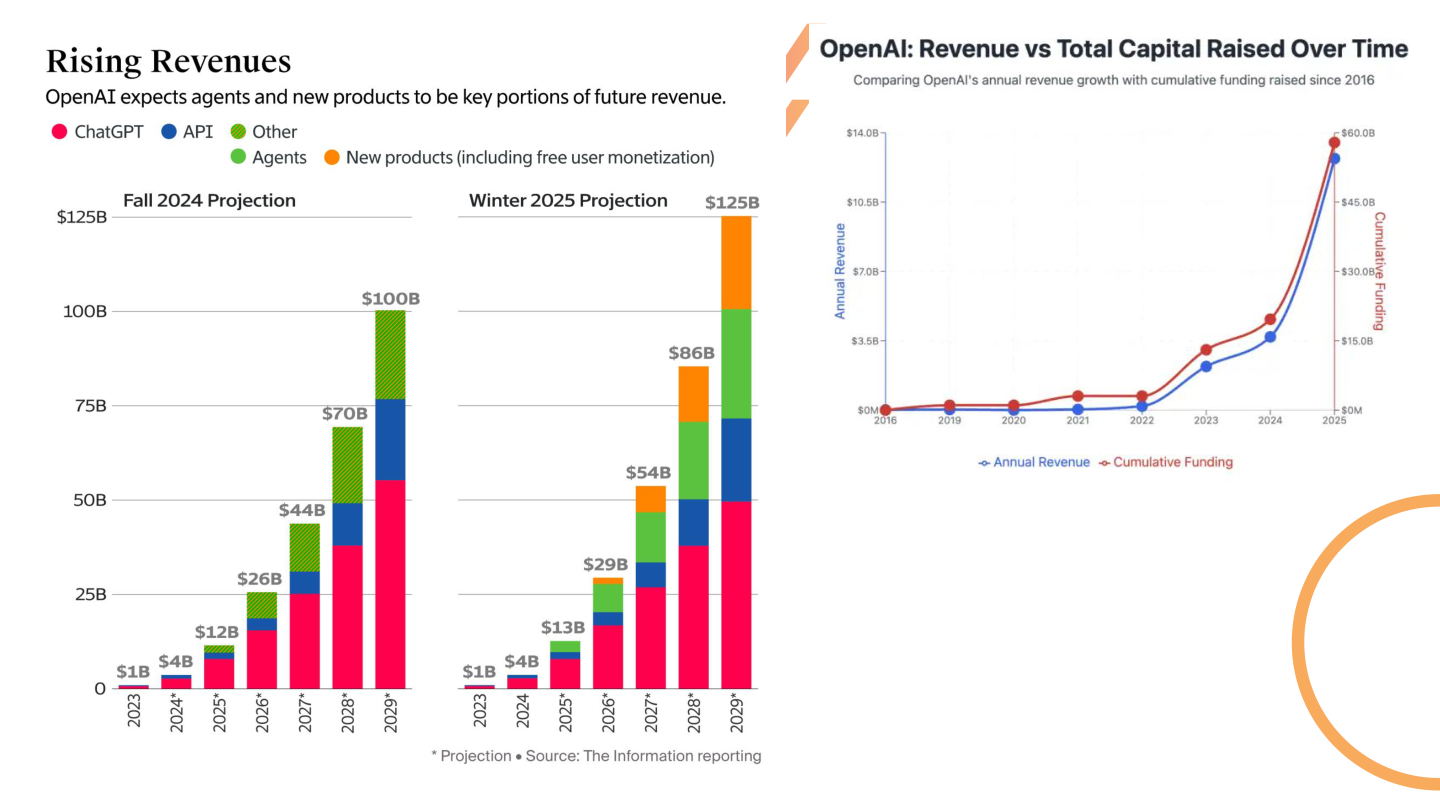

AI infrastructure is an especially important example because growth depends on enormous capital expenditure. Model labs need compute. Cloud providers need data centers. GPU suppliers need customers with the ability to absorb massive hardware purchases. The commercial story is not only about technical demand; it is also about who finances the capacity.

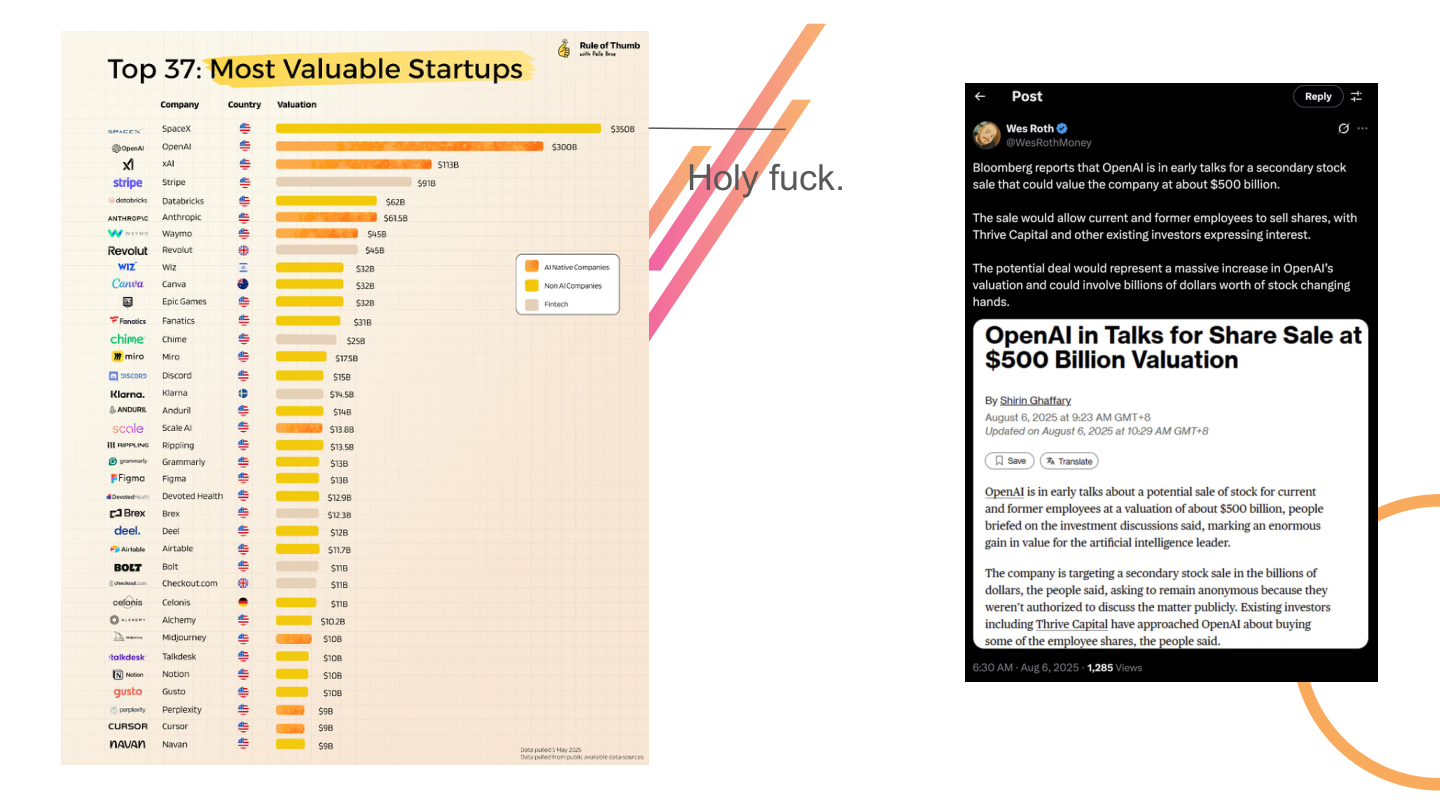

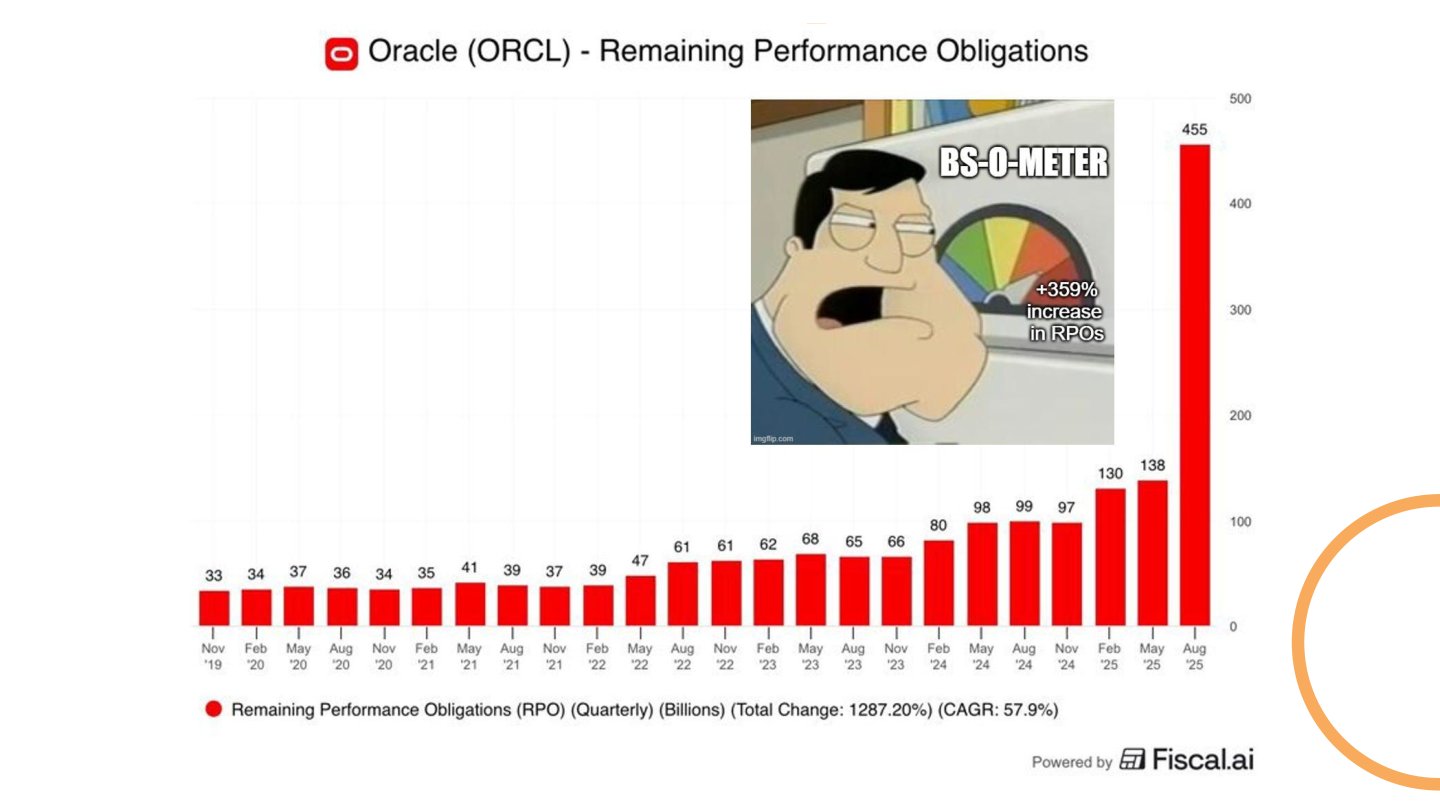

Some of the recent AI infrastructure announcements are staggering because they combine huge revenue expectations with huge counterparty risk.

When a company signs hundreds of billions of dollars in compute commitments, the diligence question becomes recursive. The buyer needs the capacity to grow revenue. The seller needs the buyer to grow enough to honor the contract. The chip vendor may have incentives to finance the ecosystem so GPU demand keeps compounding.

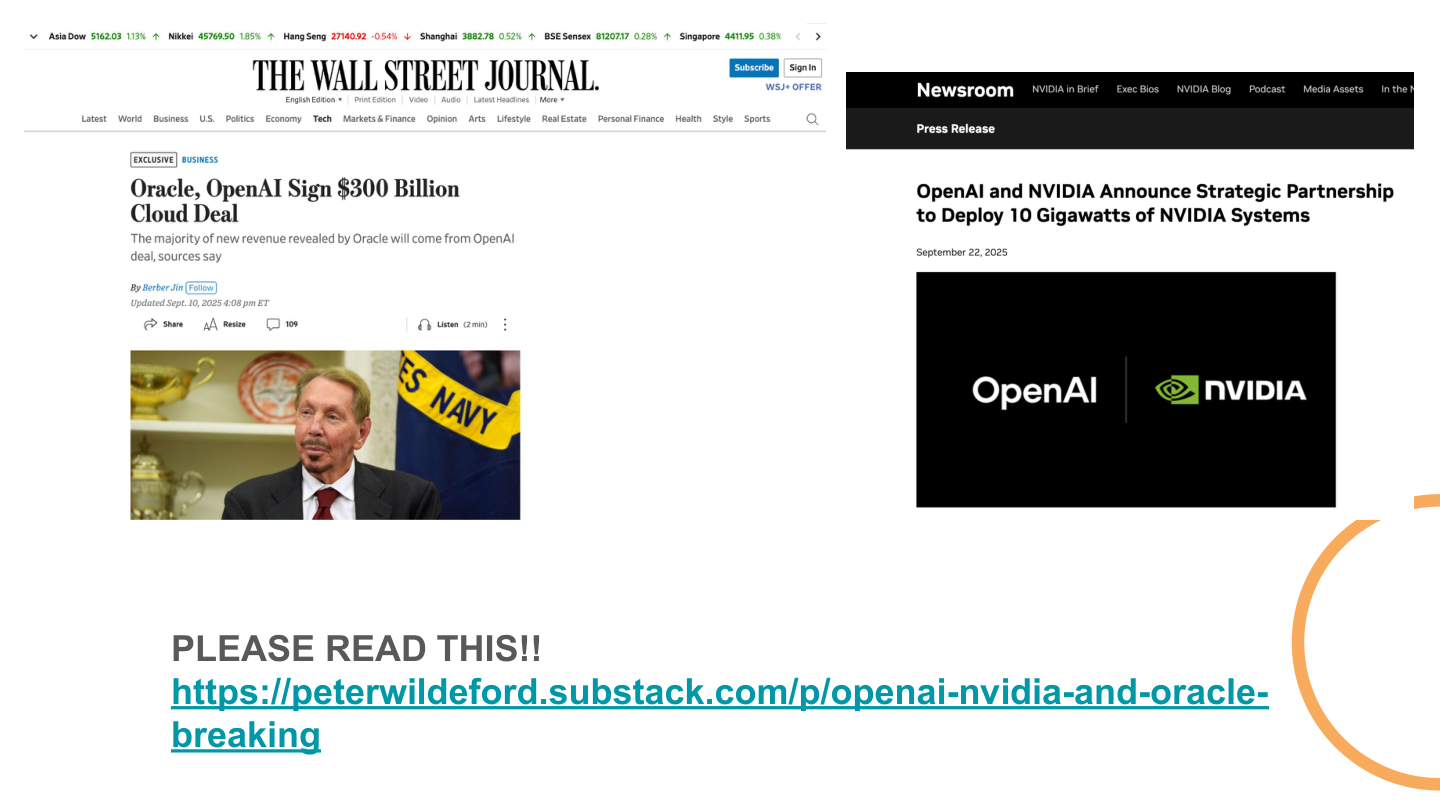

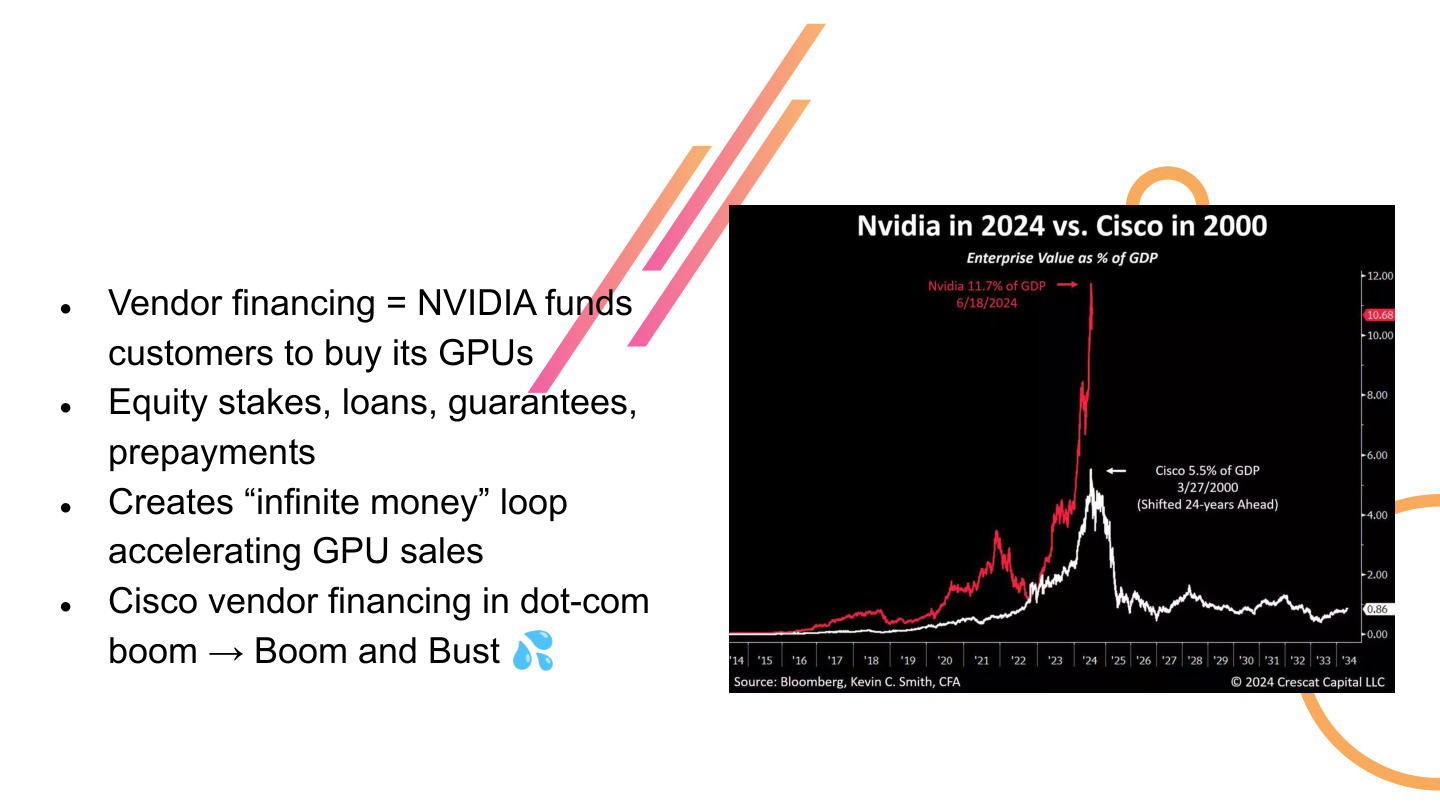

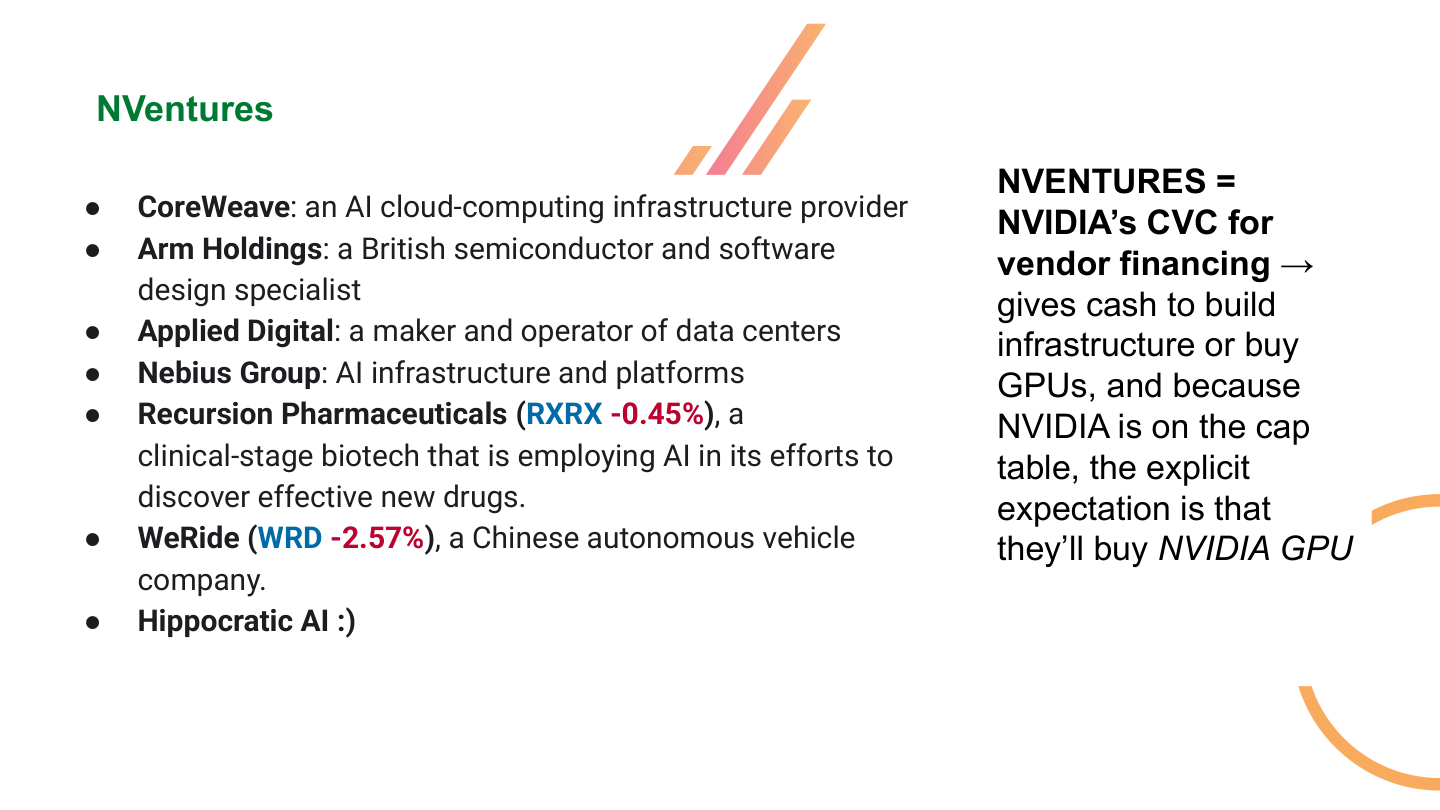

This is where vendor financing enters the story.

If NVIDIA funds or supports customers who then buy NVIDIA GPUs, the loop can accelerate reported demand. That does not automatically make the market fake. It does mean diligence has to distinguish organic end-demand from financed demand.

A single gigawatt of data center capacity can imply tens of billions of dollars over a multi-year period. These are not normal software scaling costs. AI infrastructure looks like software demand sitting on top of industrial capital intensity.

The historical analogy is Cisco vendor financing during the dot-com boom. Financing customers can pull demand forward, but it can also make the ecosystem fragile if customer economics do not catch up.

NVentures and related investments show how strategic capital can shape an ecosystem. Equity investments, guarantees, prepayments, and customer financing can all help build the market for GPUs and AI infrastructure. The diligence question is whether the resulting demand is durable once the financing loop weakens.

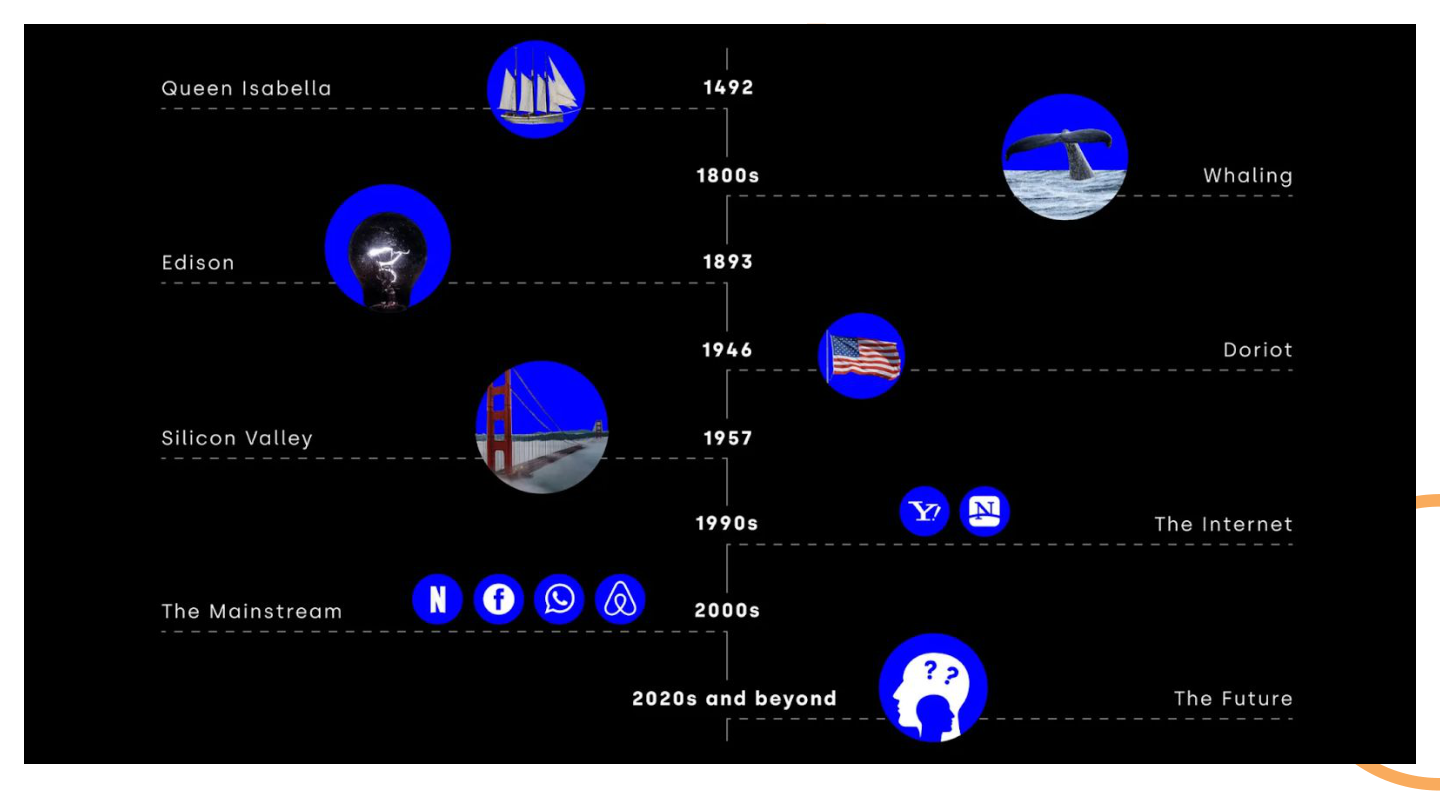

A Short History of Venture Capital

To understand where venture is going, it helps to remember that venture capital grew out of a very specific technological and geographic context.

Silicon Valley did not emerge from capital alone. It emerged from universities, defense funding, semiconductor talent, ambitious engineers, and investors willing to finance companies before the category looked obvious.

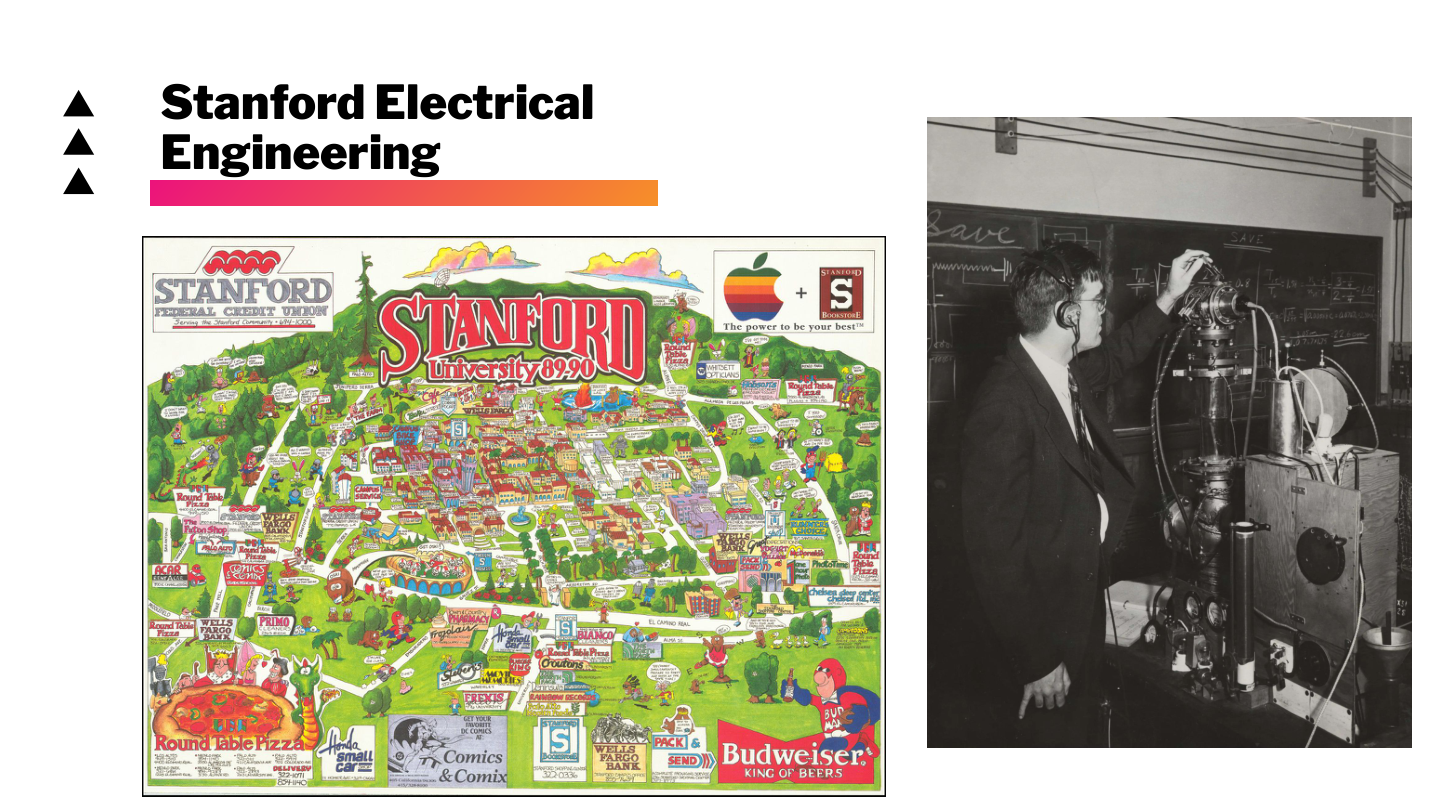

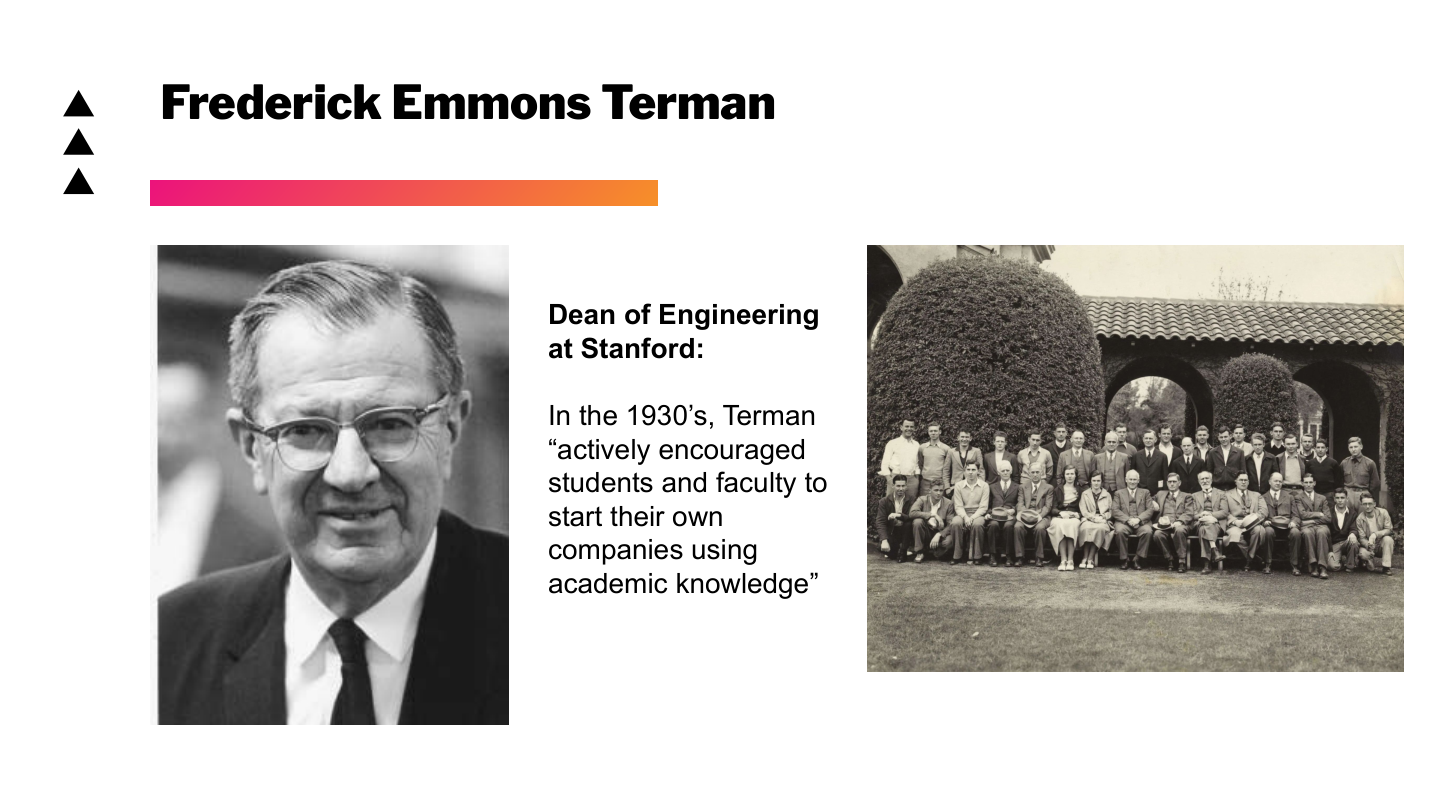

Stanford’s engineering culture mattered because it encouraged academic knowledge to become company formation.

Frederick Terman is central to that story. He encouraged students and faculty to start companies with academic knowledge, helping create the bridge between university research and commercial technology.

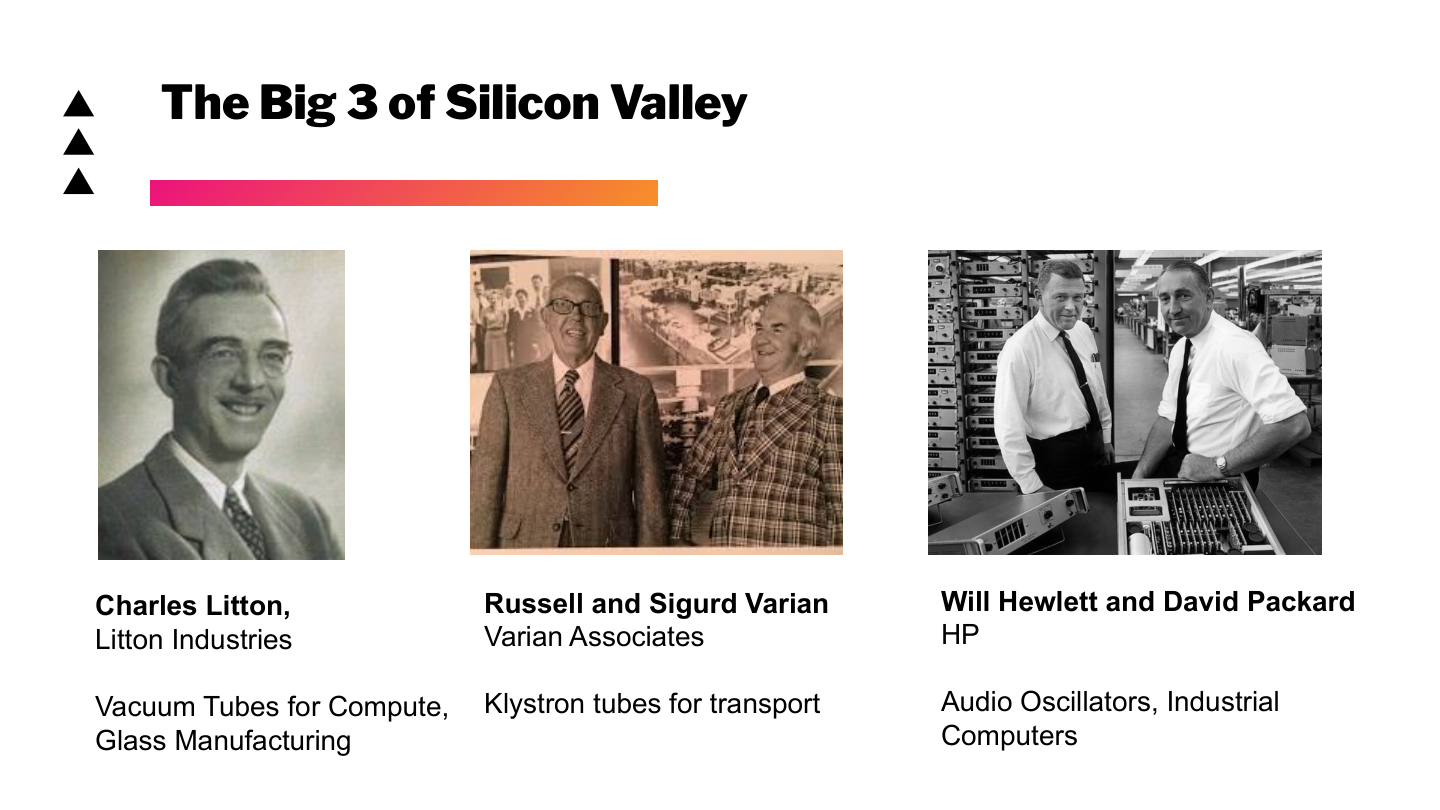

The early Silicon Valley company formation pattern shows up in firms like Litton, Varian, and HP.

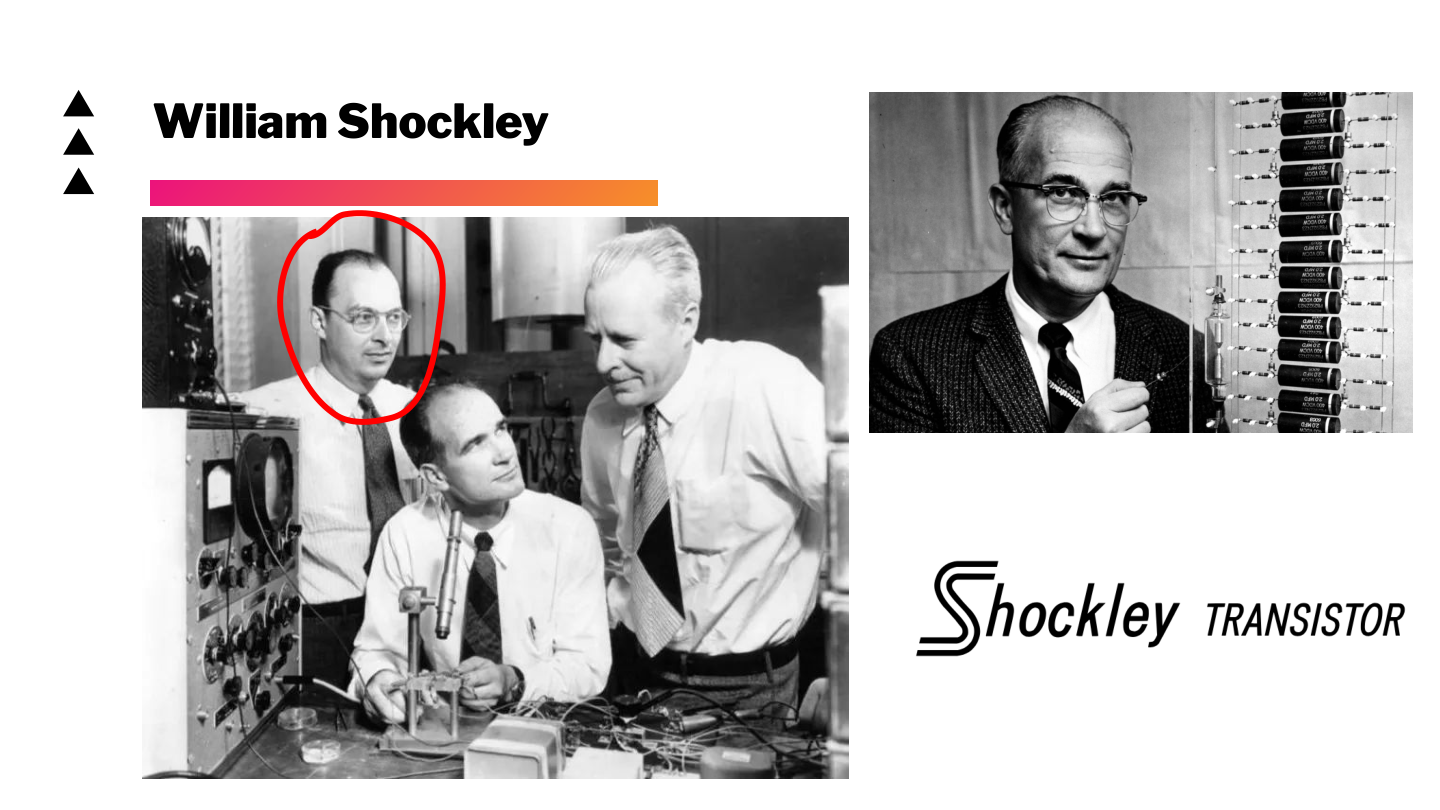

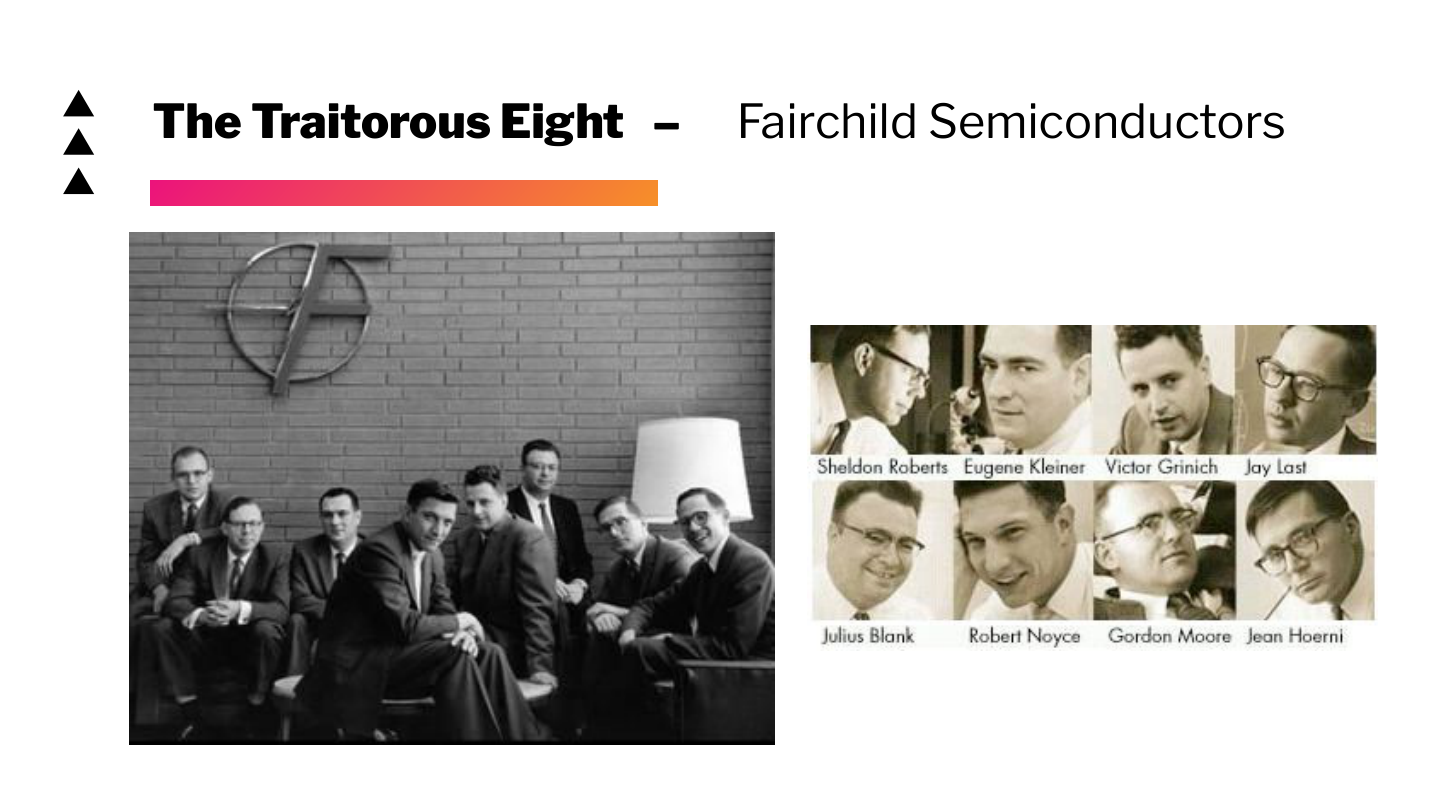

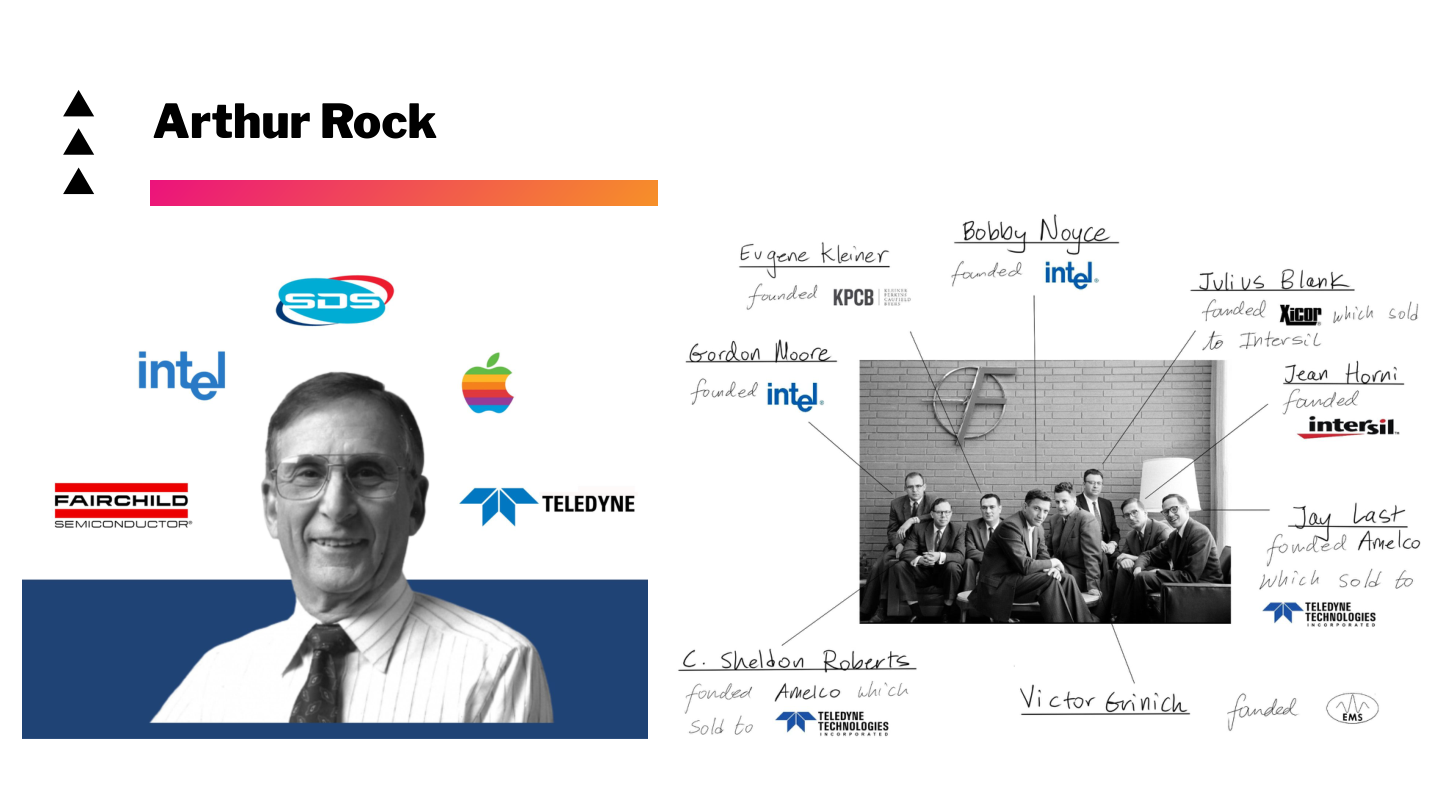

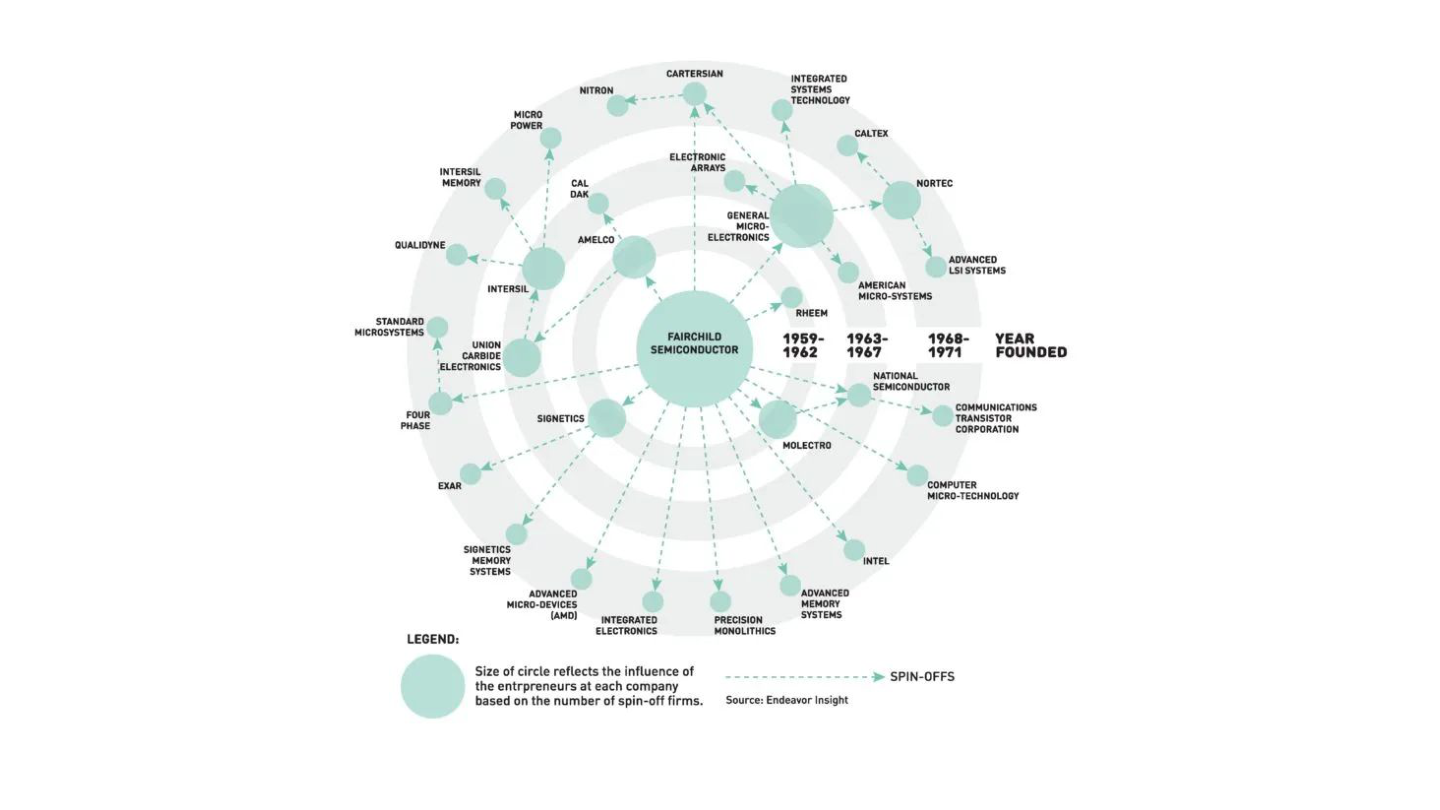

Then came the semiconductor era, including Shockley, Fairchild, and the “traitorous eight.” This was not just a story about chips. It was a story about talent mobility, company formation, and the compounding of technical communities.

Arthur Rock helped turn that pattern into an investment model.

The important idea is that venture capital was not born as a generic asset class. It was a response to a specific kind of technological uncertainty: brilliant technical teams building markets that did not yet fit traditional financing.

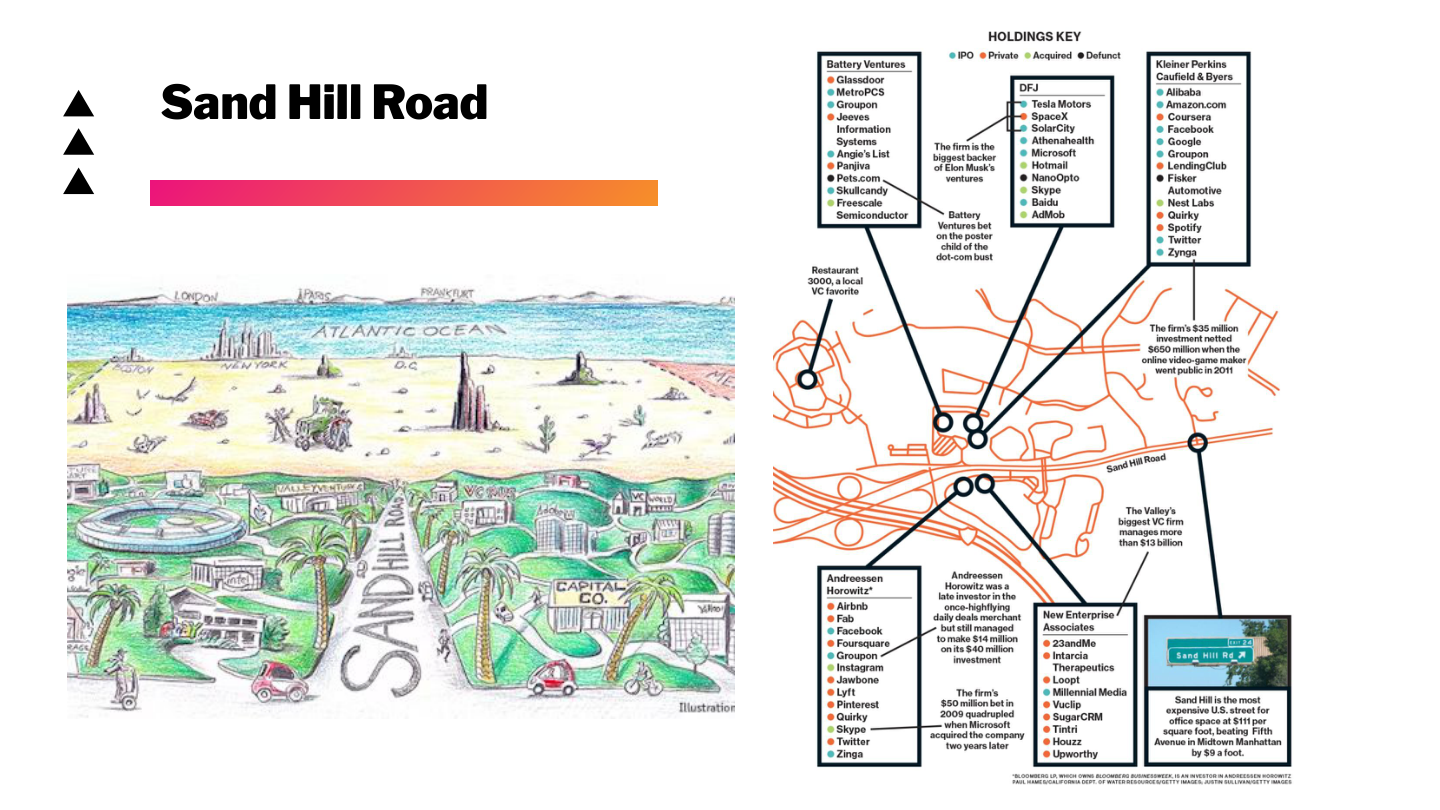

Sand Hill Road became shorthand for that financing network.

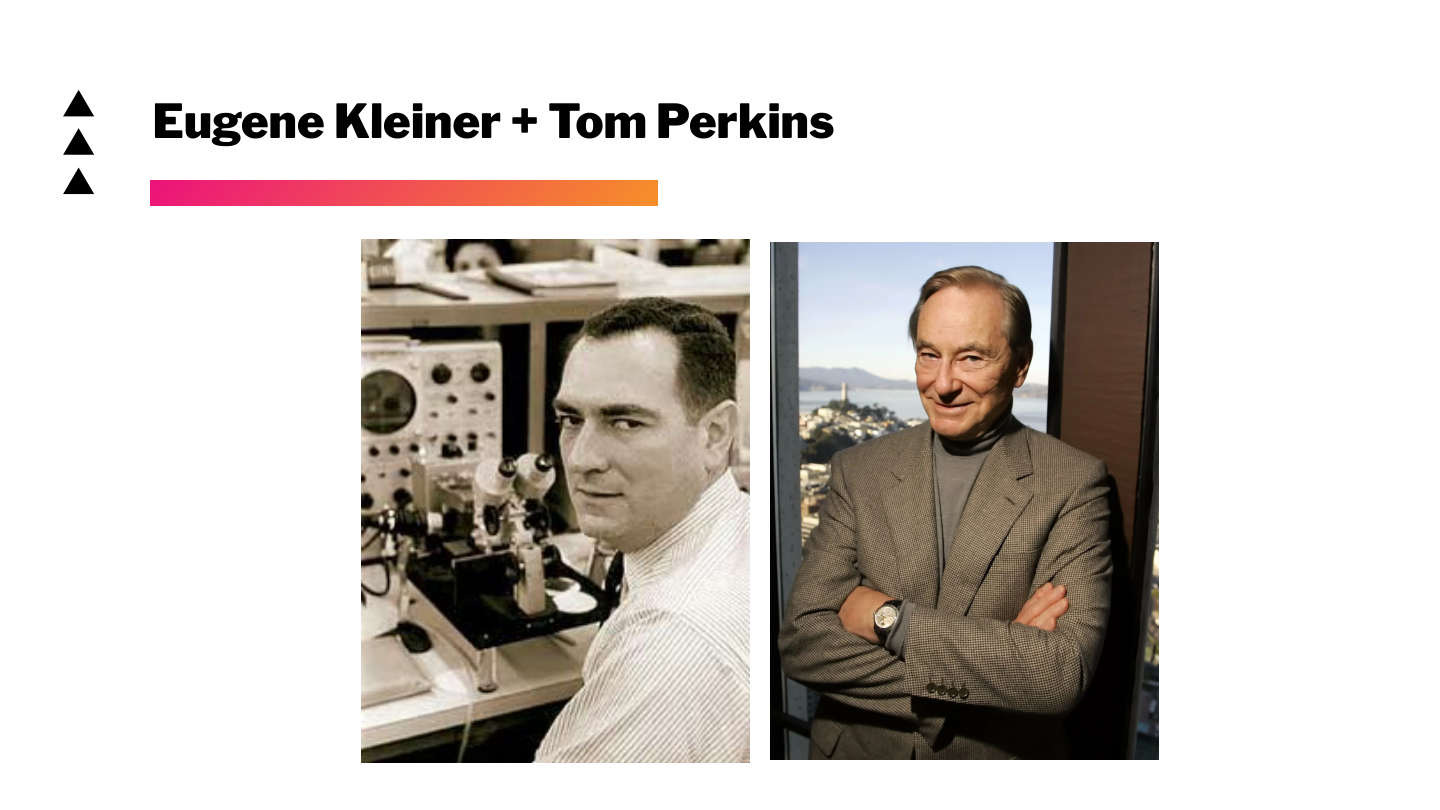

Kleiner Perkins and Sequoia institutionalized parts of the model through different investing philosophies and company-building networks.

Don Valentine and Sequoia sharpened the market-first lens: large markets can pull great companies into existence.

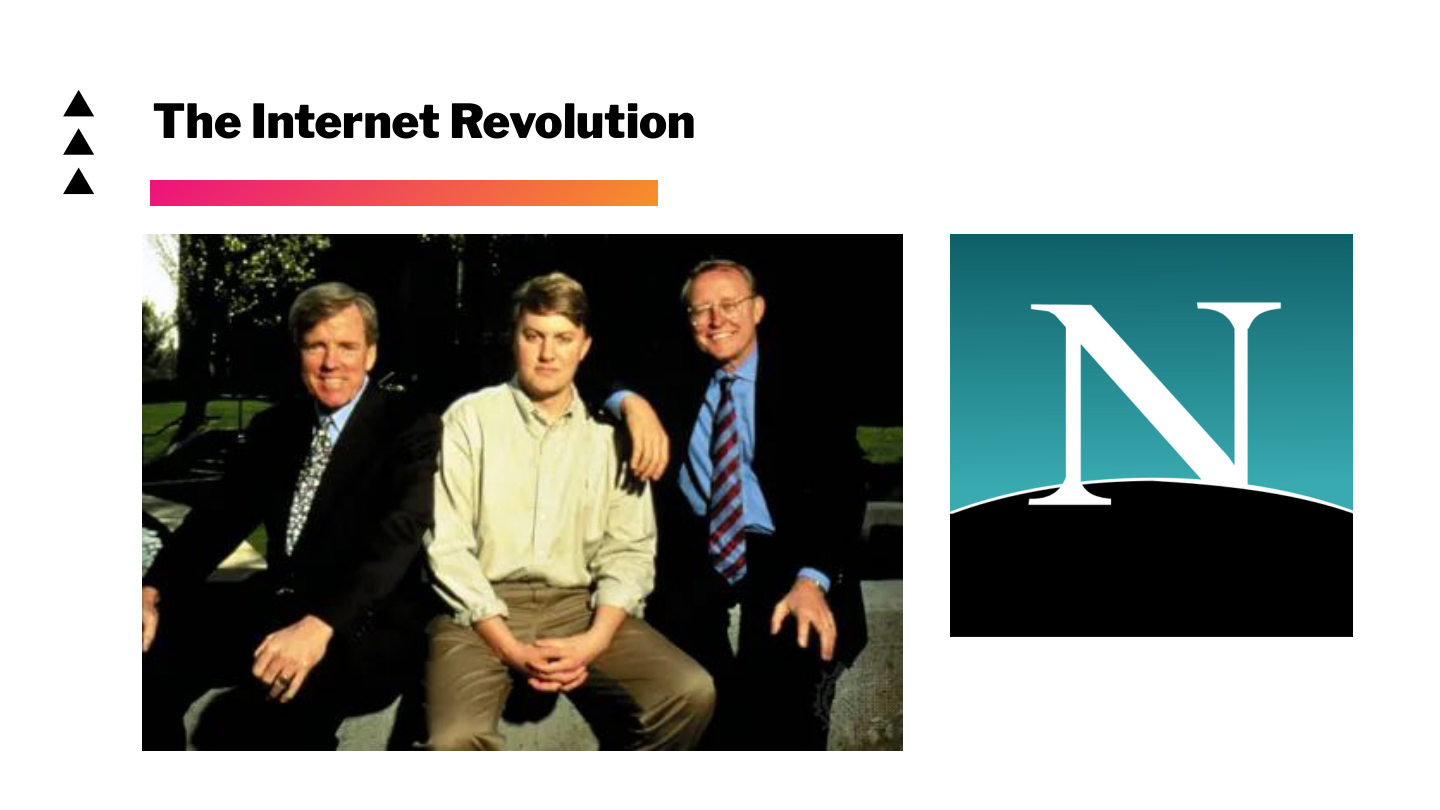

From semiconductors to the internet, venture repeatedly found itself financing platform shifts before the financial shape of those shifts was obvious.

Marc Andreessen’s “software is eating the world” essay captured the next version of that shift: software moving from a sector into an organizing layer for every industry.

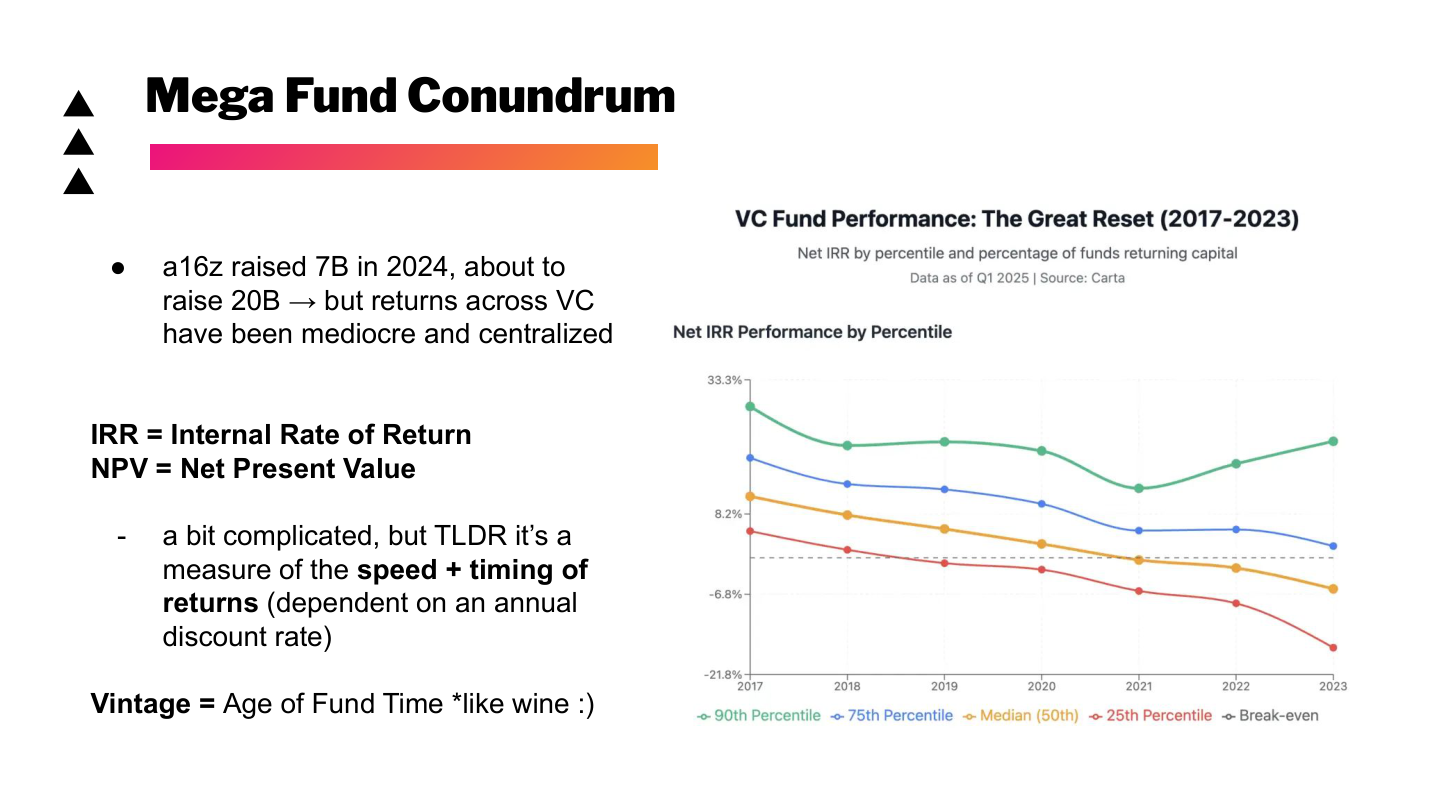

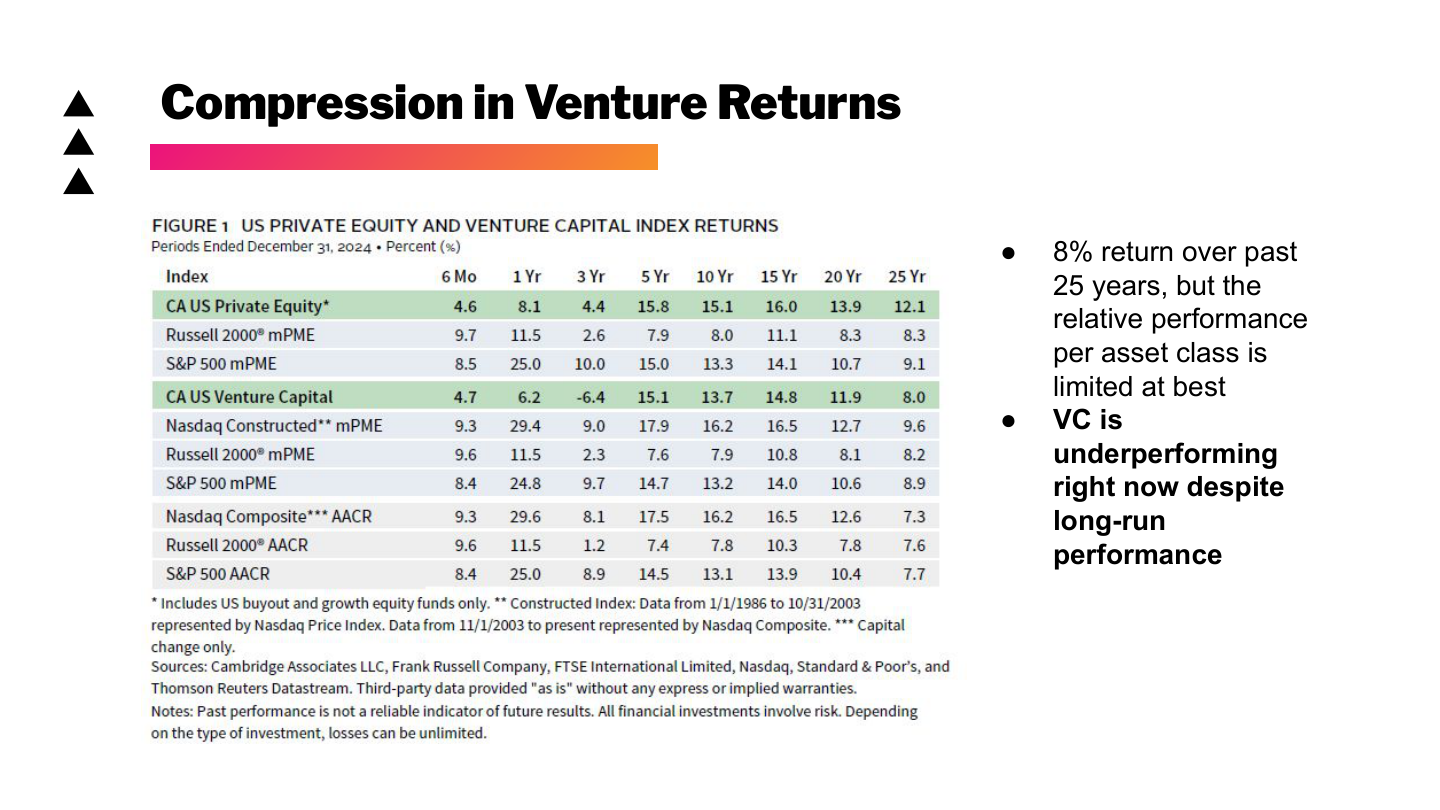

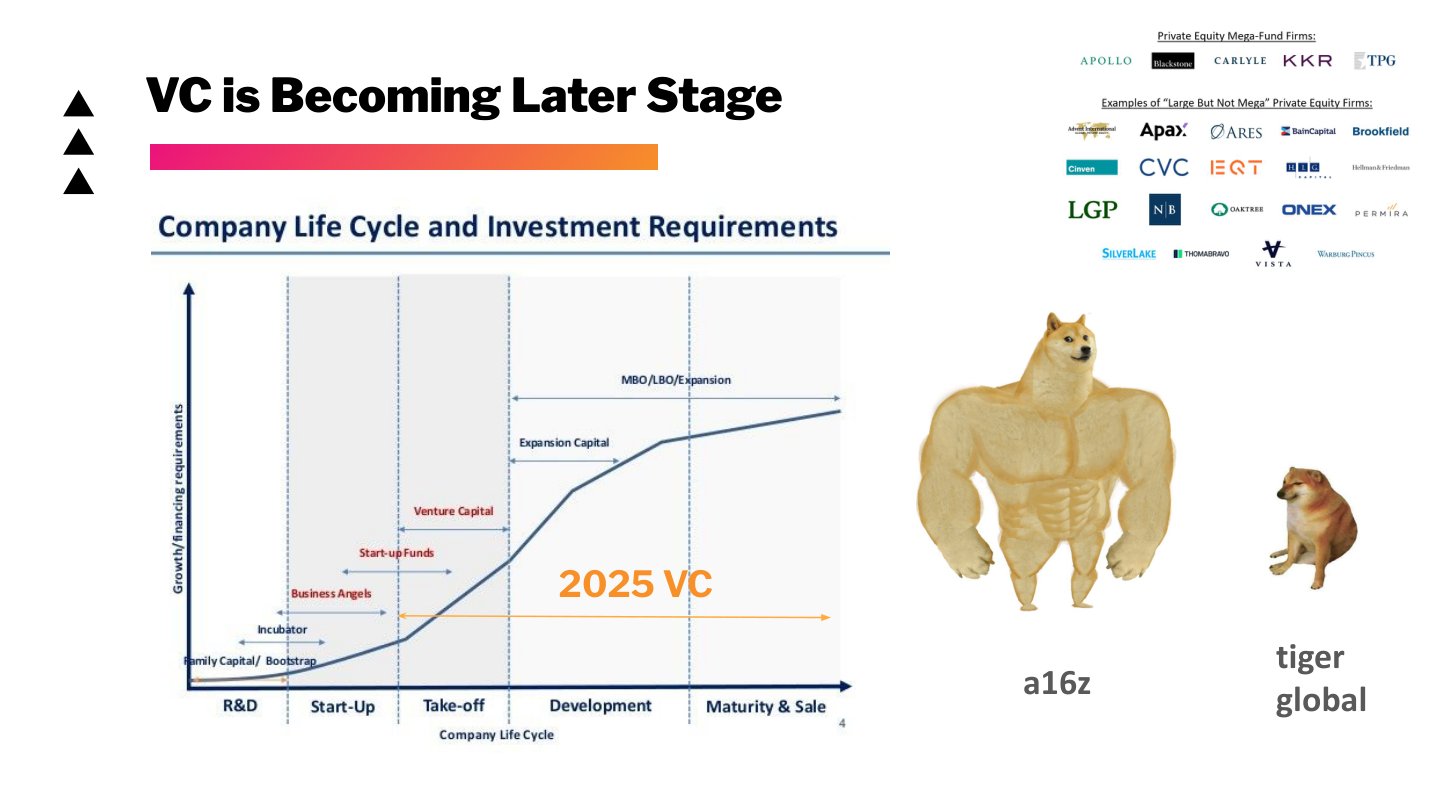

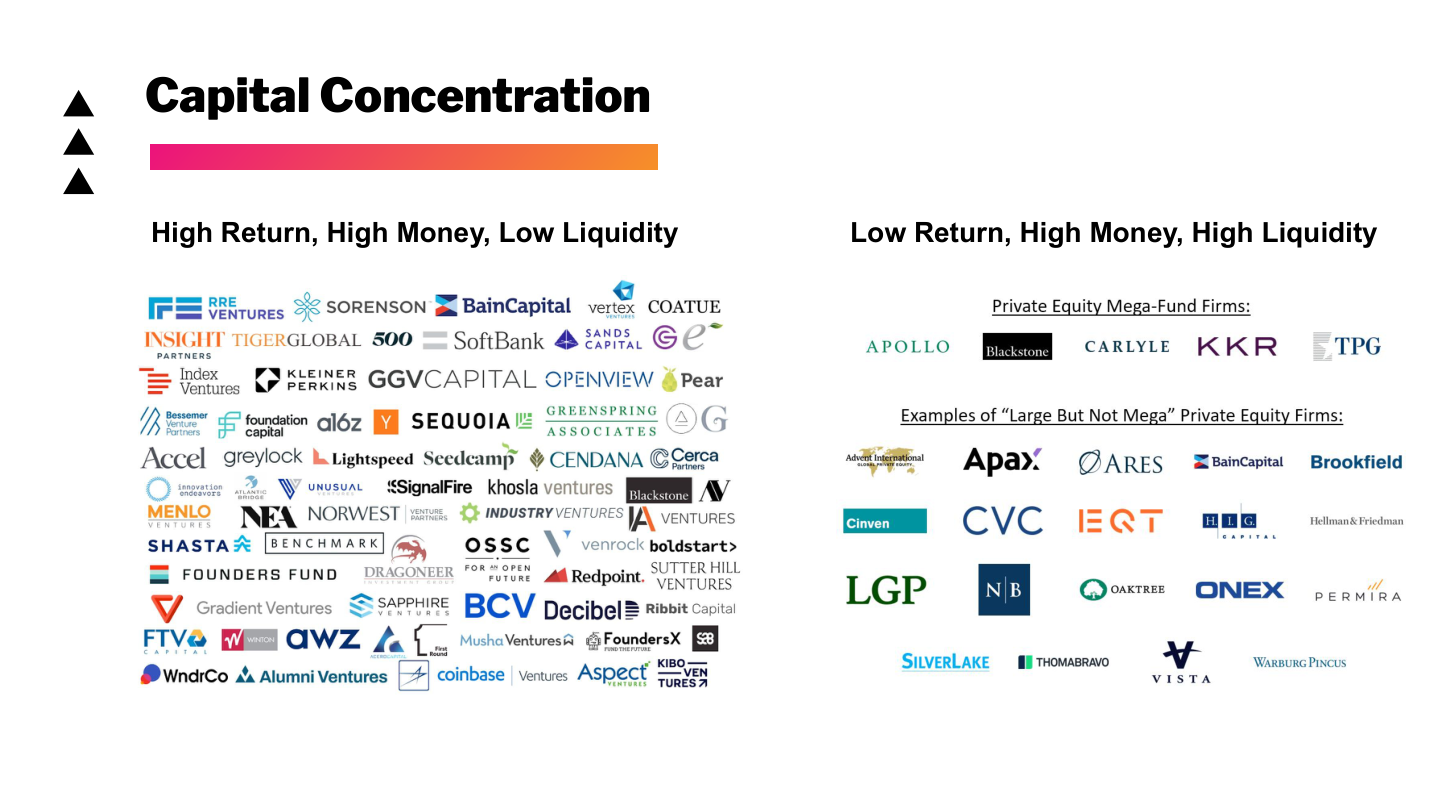

The Mega-Fund Problem

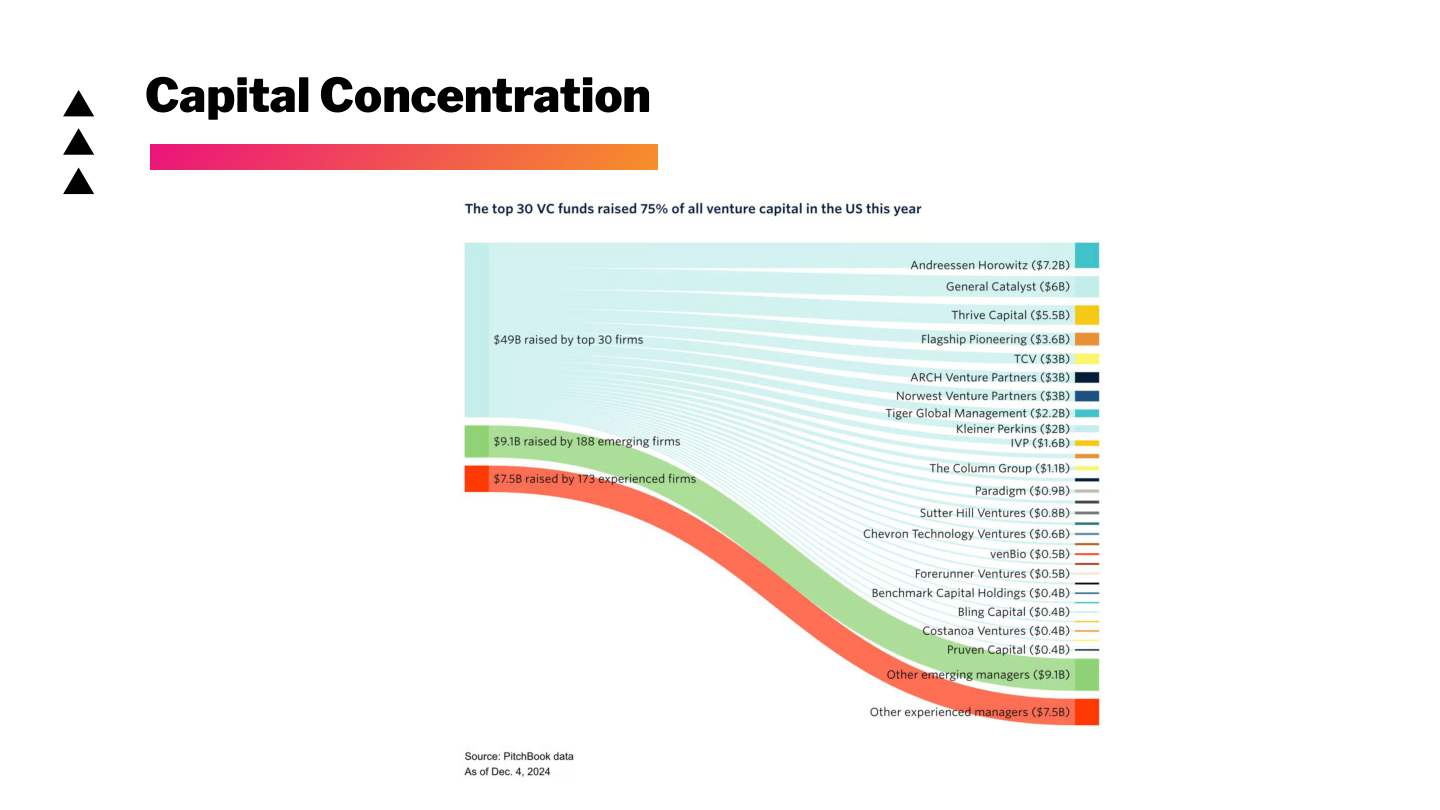

The modern venture market has a different challenge: too much capital chasing too few truly outlier outcomes.

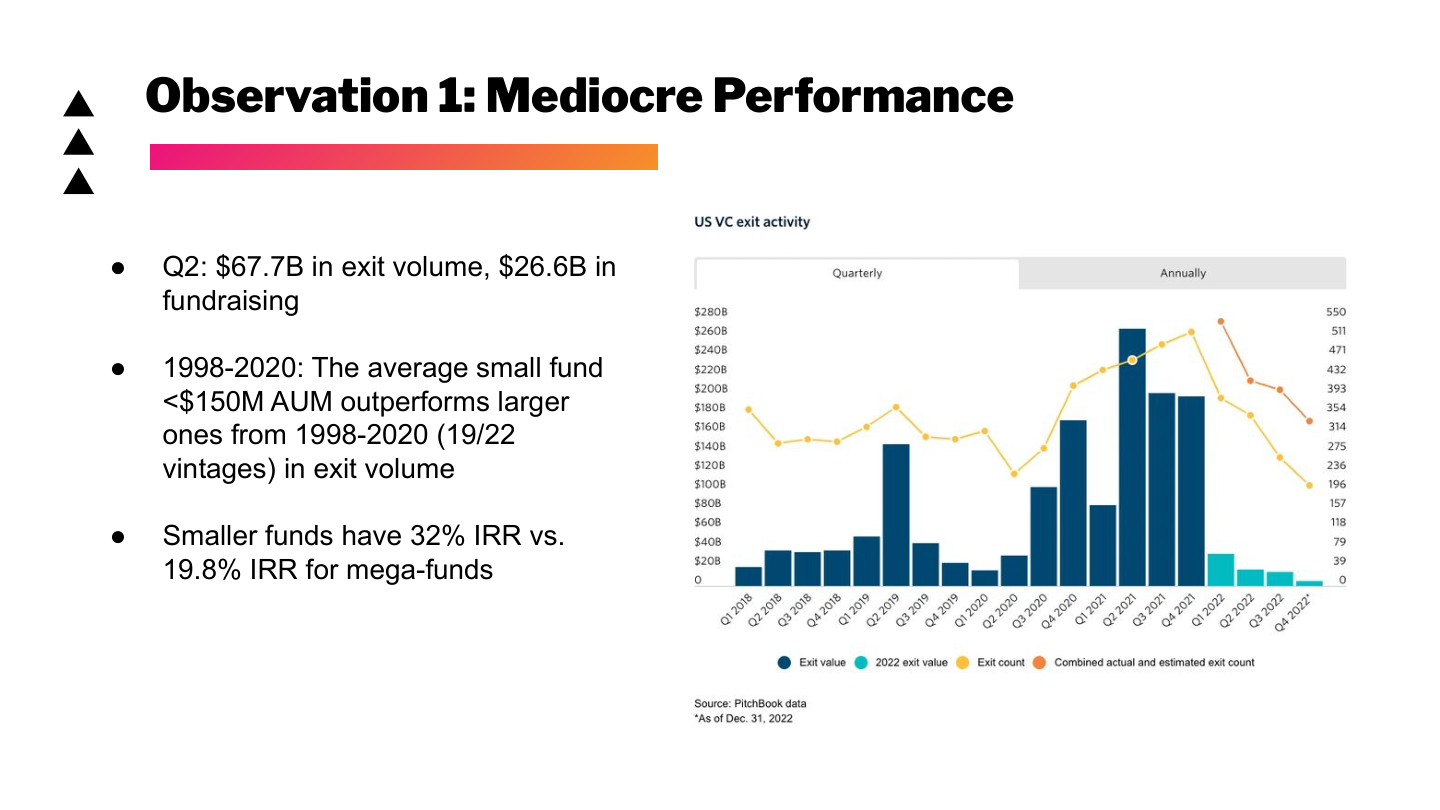

Large funds need large exits. A small fund can return capital with a handful of modestly large outcomes. A multi-billion-dollar fund needs enormous value creation just to move the needle.

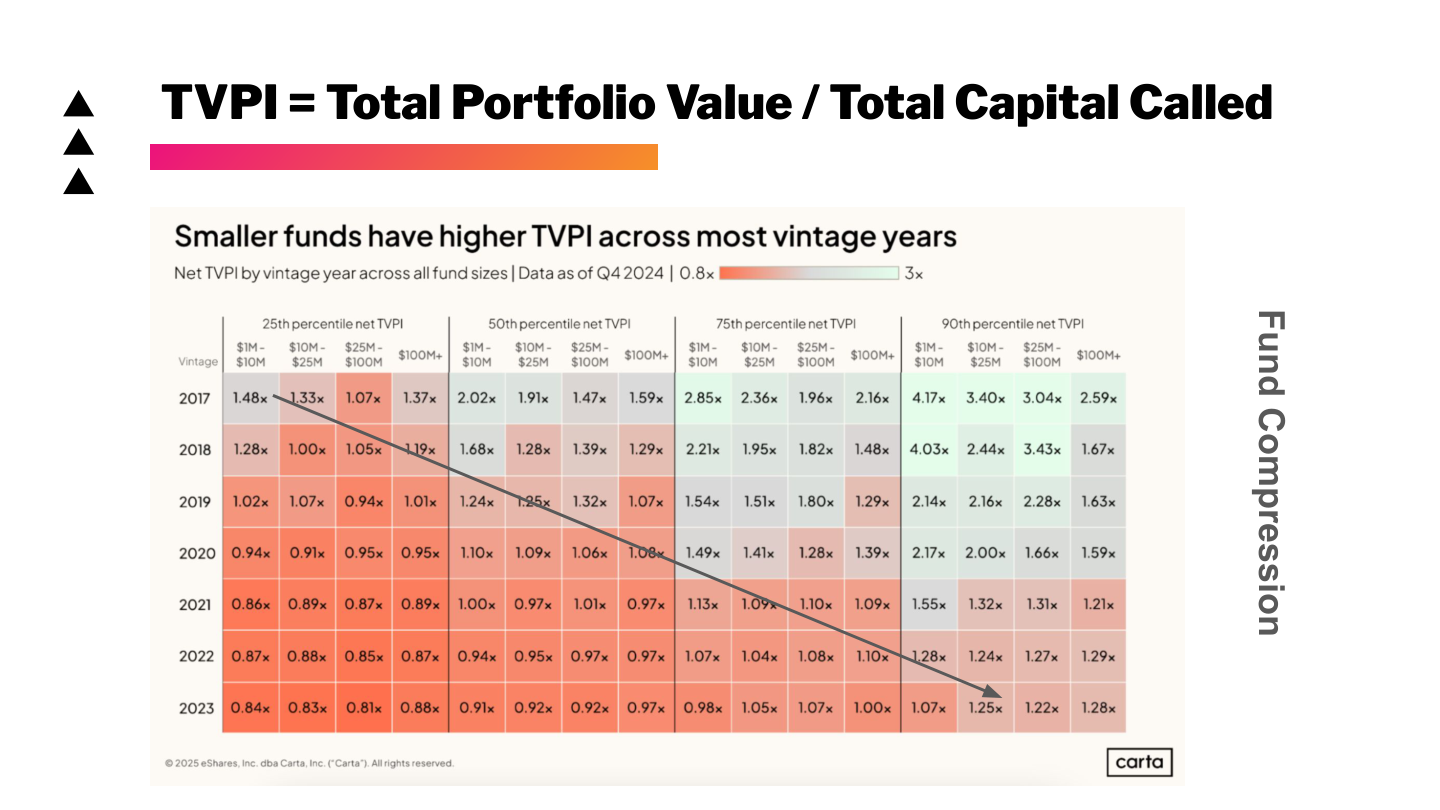

That is one reason smaller funds have historically outperformed larger ones in many vintages. The denominator matters. Returning 5x on a small fund is structurally easier than returning 5x on a giant one.

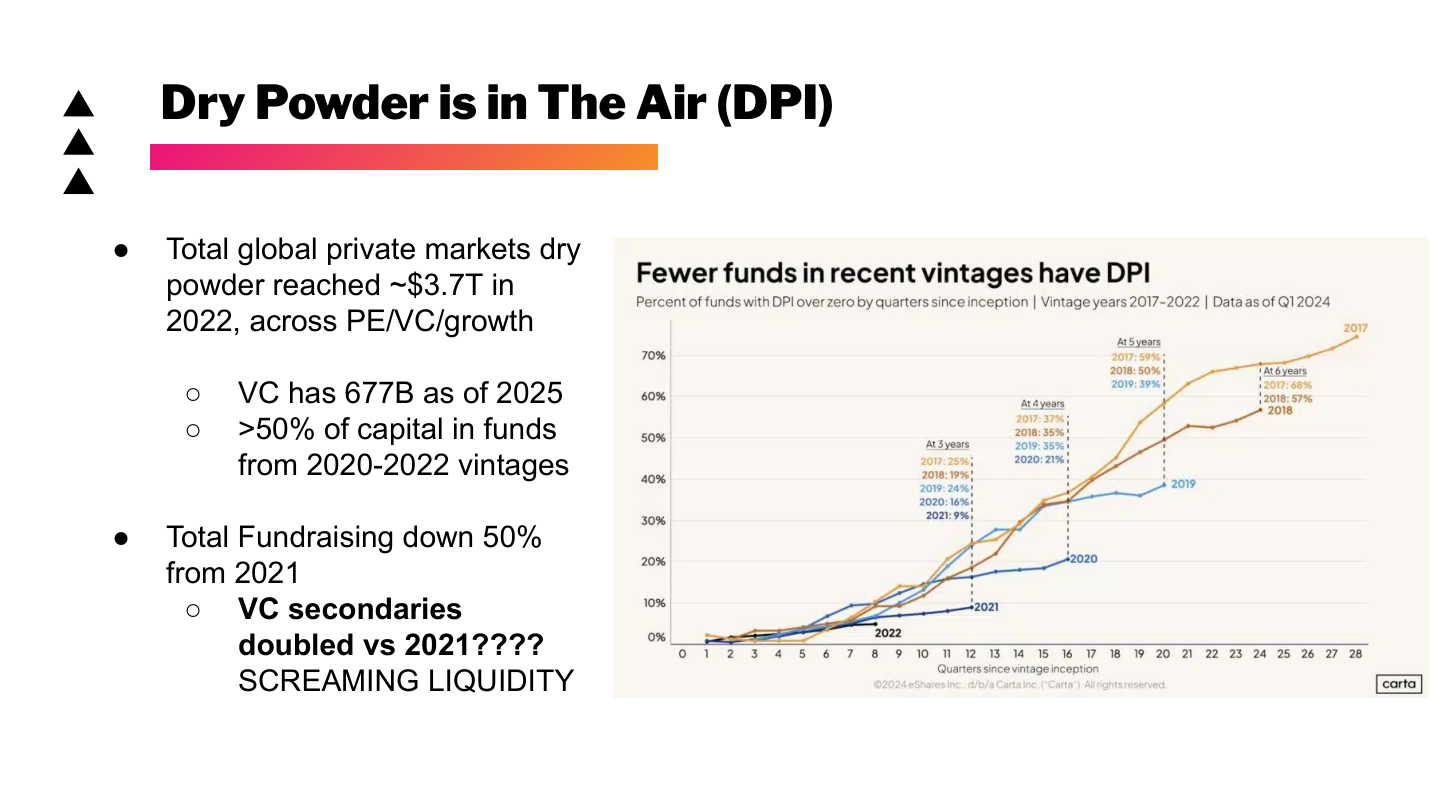

TVPI, DPI, IRR, and vintage year are not just finance jargon. They are tools for understanding whether venture capital is actually returning cash, merely marking up paper value, or compressing under the weight of its own capital base.

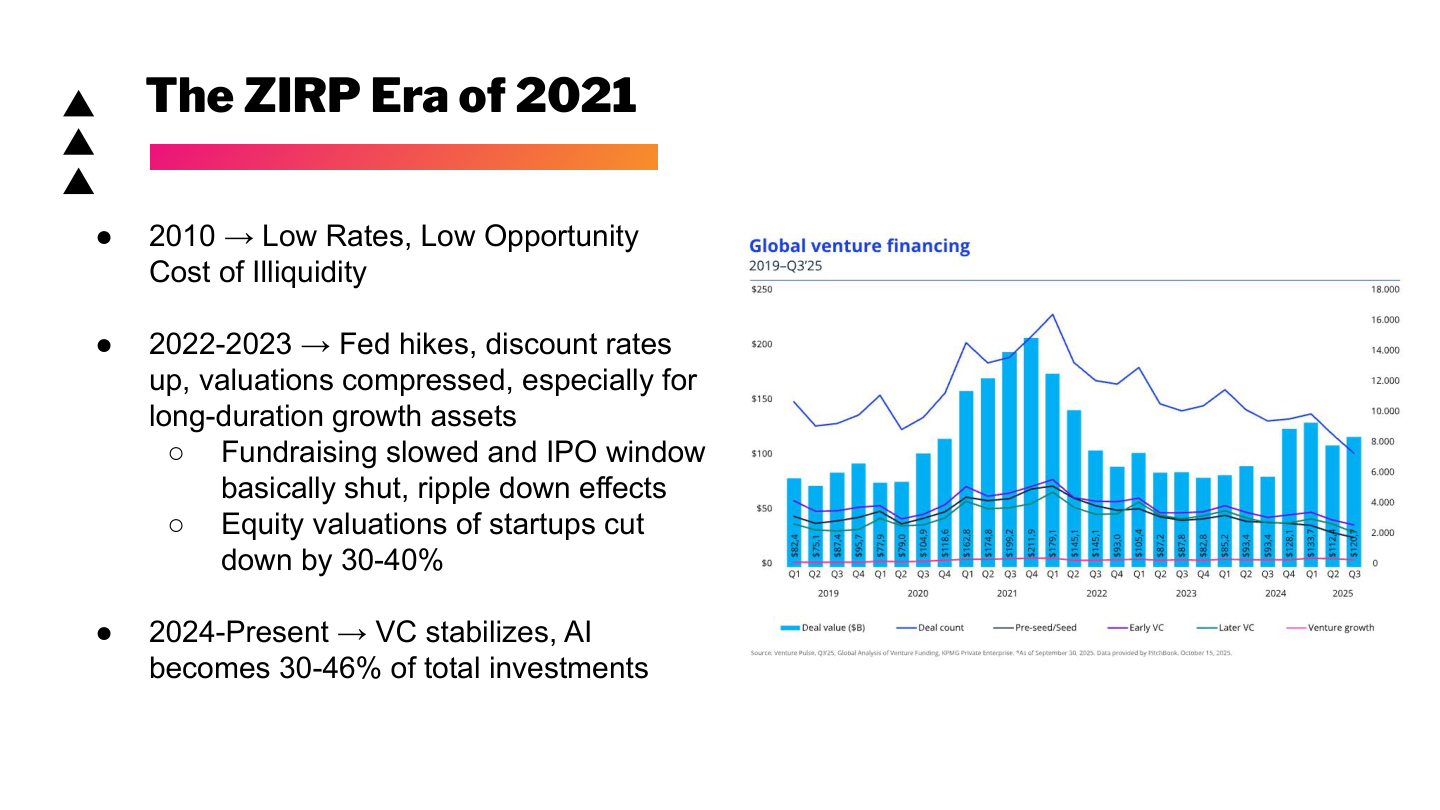

The ZIRP era made this harder. Low rates made illiquid growth assets more attractive, valuations expanded, and capital flooded into venture. When rates rose, long-duration growth assets repriced, the IPO window narrowed, and fundraising slowed.

Dry powder remains high, but liquidity is tighter. That creates a strange market: lots of committed capital, fewer exits, more secondaries, and more pressure to find companies that can absorb enormous rounds.

Power Laws and Capital Concentration

Venture has always been power-law distributed, but fund size changes how the power law feels.

If a fund raises $5 billion and aims for a 5x net return, it needs outcomes that are almost absurdly large. That pushes capital toward later-stage companies where the category winner seems more visible, even if the entry price is higher.

As a result, venture capital begins to look more like growth capital in parts of the market.

Capital concentrates in companies that already look like winners, while early-stage investors compete over whether they can still underwrite enough ownership before the outcome becomes obvious.

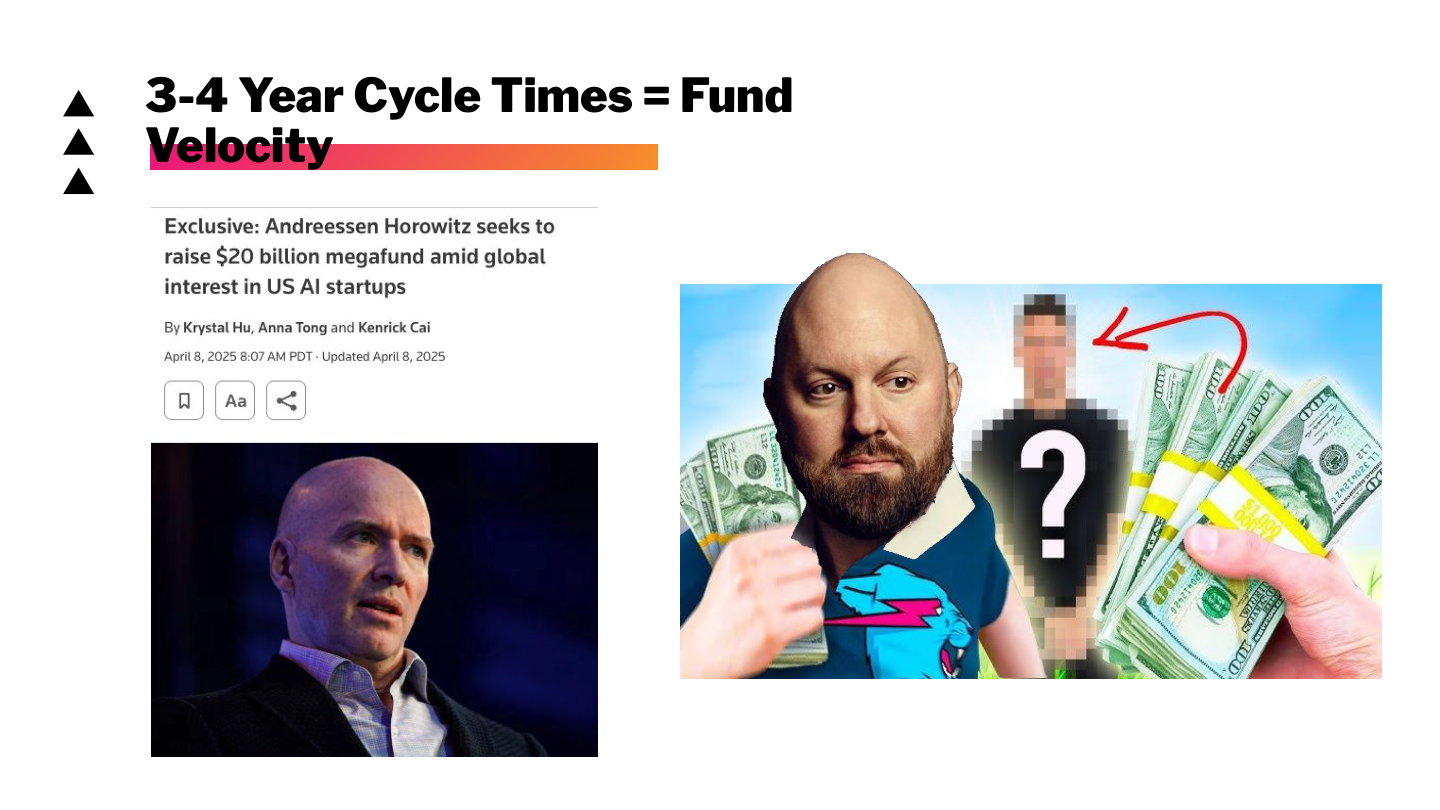

Fund velocity also matters. The three-to-four-year cycle of raising, deploying, marking, and raising again can distort behavior. Investors need to show progress before the underlying companies have fully matured.

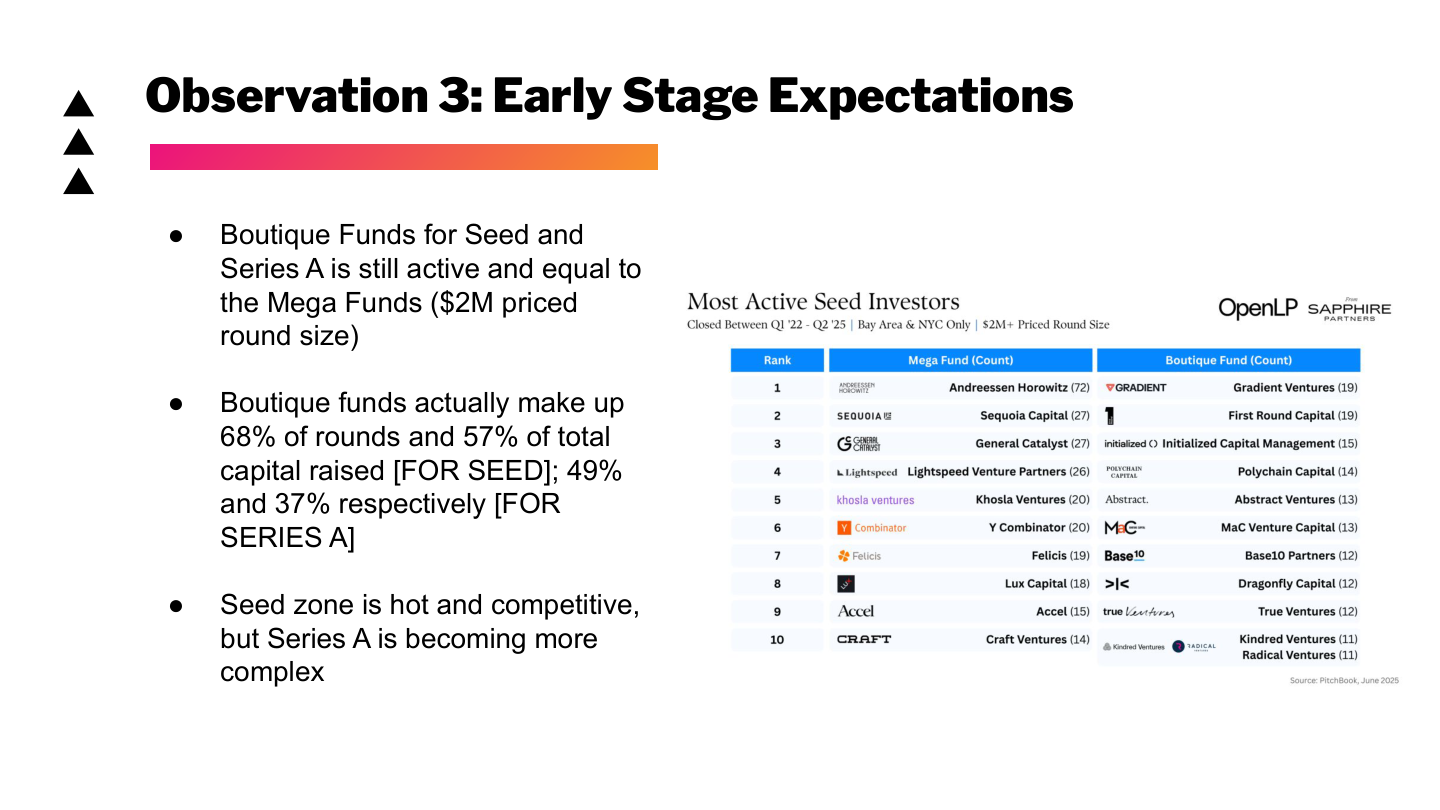

Early Stage Still Matters

Despite all of this, early-stage venture is not dead. Boutique funds still play an important role at seed and Series A because they can write smaller checks, take sharper views, and return capital from outcomes that would not move a mega-fund.

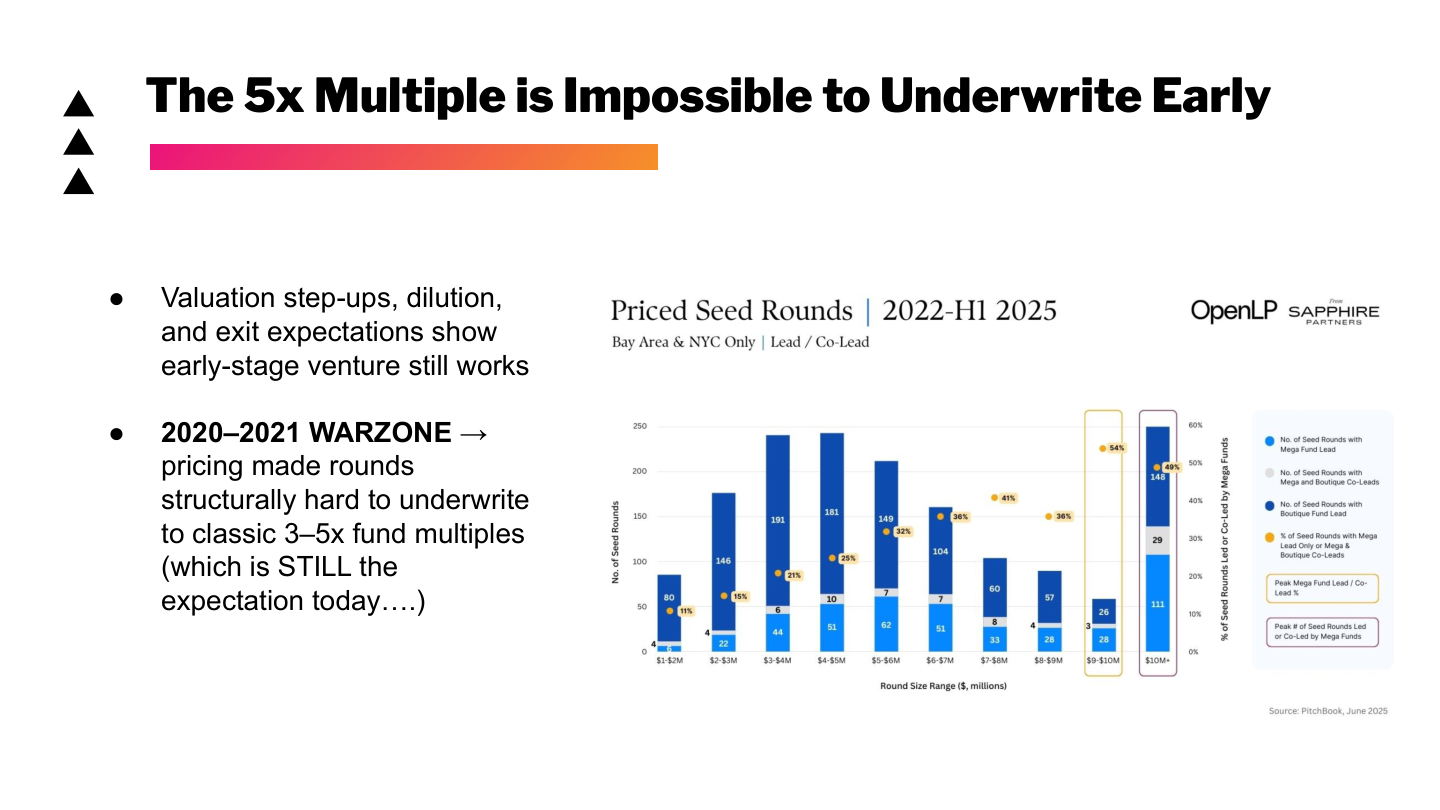

The difficulty is underwriting. Early-stage investors are still expected to believe in 3x to 5x fund outcomes, but pricing, dilution, and exit expectations can make that math fragile, especially when entry valuations are inflated.

So will venture capital last? Probably, but not unchanged.

The future likely looks more barbelled. Large pools of capital will continue to chase late-stage category winners and AI-scale infrastructure outcomes. Smaller funds will keep hunting for overlooked early-stage companies where ownership, entry price, and founder support still work. In between, more hybrid models will emerge: secondaries, accelerators, platform services, rolling funds, and firms that blend capital with distribution or company-building help.